If you’re researching florida condo special assessment 2026, the biggest takeaway is simple: a low monthly HOA fee does not always mean a lower true cost of ownership. In Miami-Dade, Broward, and Palm Beach, condo buyers, sellers, and investors need to review reserves, inspection reports, and board records before they commit to a closing.

SB 4-D

Florida Condo Safety Law

$5K+

Typical Lower-End Assessment Range

$200K+

Typical High-End Assessment Range

Key takeaway: A special assessment is often not the surprise itself — it’s the lack of early due diligence that turns it into an expensive problem.

Florida Condo Special Assessment 2026: What It Means for Buyers

A special assessment is an additional charge that a condo association can impose on unit owners when regular monthly dues and reserves are not enough to cover a major expense. These are usually tied to capital needs, safety work, or a funding gap that the board cannot ignore any longer.

Special assessments can happen for many reasons: major repairs, deferred maintenance, structural upgrades, waterproofing, roof work, elevator replacement, or other large projects that go beyond the association’s normal operating budget. In practice, the risk rises when a building has postponed needed work for too long or when reserve funding has not kept pace with real repair needs.

Important: A condo can look beautifully maintained and still carry a hidden assessment risk if reserves are weak or major projects are already being discussed in the minutes.

Warning: Low HOA dues are not proof of a healthy building. They can also signal deferred maintenance, underfunded reserves, or a future cash call.

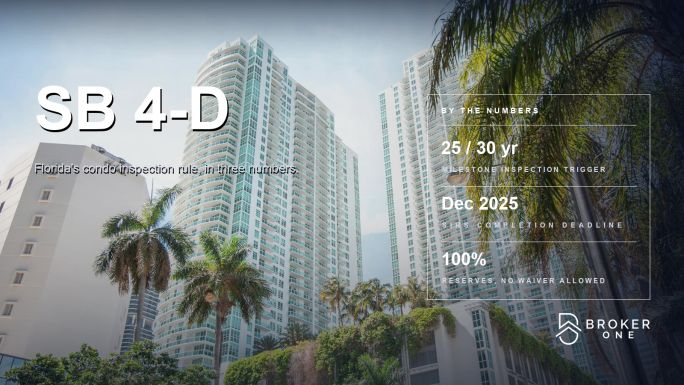

Florida SB 4-D and Why Condo Safety Rules Matter More in 2026

Florida’s post-Champlain Towers condo safety framework, including SB 4-D, pushed structural condition and reserve planning to the top of every serious buyer’s checklist. As you evaluate a condo, the key issue is not just whether the building looks good today — it’s whether the association has documented the building’s long-term repair needs and funding plan.

One of the most important parts of that conversation is the structural integrity reserve study. For certain buildings, this study is meant to identify major components that will need future funding and to help the association plan responsibly instead of relying on emergency assessments later.

Key takeaway: A reserve study is only valuable if the association is actually funding what the study shows. A report without action can still leave owners exposed.

Pro tip: When you review a building in Miami-Dade, Broward, or Palm Beach, ask whether the condo has a current structural integrity reserve study and whether the budget reflects it.

How to Check for Pending Assessments Before You Buy

If you want to avoid walking into a surprise bill, don’t rely on verbal reassurances from the listing agent. You want written evidence. Start with the association documents, then verify the building’s condition and permit history.

- Request the condo association disclosure package. Ask for financial statements, budgets, board minutes, reserve information, and any notices of special assessments.

- Read the last several board minutes. Look for discussion of repairs, reserve shortfalls, engineering reports, or votes tied to large projects.

- Review the reserve study. Confirm whether the building has one, whether it is current, and whether the budget actually funds the items identified.

- Check for pending work orders and repair bids. If the board is soliciting contractor bids, the assessment risk may already be active.

- Cross-check permit and violation data. Use brokerone.io for building permit and violation data, and review neighborhood-level context at Broker One neighborhoods.

- Review the purchase contract carefully. Make sure the contract addresses any existing or anticipated assessment before you sign.

Due diligence shortcut: If the association is slow to provide documents, that delay itself is a warning sign. Good buildings are usually organized when buyers ask for records.

Documents to Request from the HOA or Condo Association

- Current budget

- Most recent financial statements

- Reserve study and any updates

- Board meeting minutes from recent months

- Special assessment notices, if any

- Engineering reports

- Insurance summary

- List of pending or approved capital projects

- Estoppel or payoff information for the unit you want to buy

- Any disclosure about unpaid assessments tied to the property

Typical Special Assessment Costs in South Florida

Special assessments in South Florida can vary widely, and the range you should budget for can move from $5K+ to $200K+ depending on the scope of the work, the age of the building, the condition of the reserves, and how quickly the association needs the money.

For a buyer, the point is not to guess the exact charge in advance. The point is to determine whether the association has a realistic funding plan or whether the building is likely to pass a large bill to owners later.

| County |

What to Scrutinize |

Why It Matters |

| Miami-Dade |

Structural reports, reserve study, permit history, violation history |

Helps you understand whether the building is carrying deferred maintenance or unresolved safety issues |

| Broward |

Board minutes, repair backlog, assessment history, current funding plan |

Reveals whether recurring repairs may turn into another cash call |

| Palm Beach |

Reserve funding, special assessment notices, seller payoff status |

Helps you avoid inheriting surprise costs at closing |

Buyer mindset: In condo ownership, the cheapest monthly payment is not always the safest purchase. Total cost matters more than the sticker price of dues.

How Reserves Work — and Why They Matter

Reserves are the association’s planned savings for major future repairs and replacement items. Instead of charging owners only when something breaks, the board collects money over time so the building can pay for larger projects when they come due.

When reserves are healthy, a building has more flexibility. When reserves are too low, the association may need to raise dues, defer maintenance, borrow, or issue a special assessment. That is why reserve funding is one of the clearest signals of whether a building is financially prepared.

Critical alert: If the minutes show major repair discussions but the budget does not show realistic reserve funding, the risk of a future assessment goes up fast.

Common Red Flags in HOA Financials

- Reserve study is missing, outdated, or ignored

- Board minutes repeatedly mention the same repairs

- Deferred maintenance appears in multiple documents

- Large projects are discussed without a clear funding source

- Frequent special assessments appear in the building’s history

- Association documents are slow to produce or incomplete

How to Negotiate a Special Assessment When Buying

You may not be able to eliminate an assessment, but you can often negotiate around it. The best strategy depends on whether the assessment is already approved, still being discussed, or likely to happen soon.

- Ask the seller to pay it at closing if the assessment is already known.

- Request a credit or price reduction equal to the likely cost impact.

- Negotiate a closing holdback if the final amount is still unclear.

- Do not waive document review just to move faster.

- Ask your lender and title company how they want the assessment handled in escrow.

As a general rule, if the assessment exists before closing, do not assume it disappears. The purchase contract and closing documents matter, and the responsibility can be handled in different ways depending on the deal.

Key takeaway: If a special assessment is already on the table, treat it like a real financial term of the contract — not a side note.

Pro tip: Buyers in Miami-Dade, Broward, and Palm Beach should use the condo documents plus permit and violation data from Broker One to support their negotiation.

Questions to Ask Before Buying a Condo in South Florida

Use these questions to separate a strong building from one that may surprise you later:

- Has the association issued any special assessments in the past?

- Is there a current structural integrity reserve study?

- Are reserves being funded in line with the study?

- What major repairs are discussed in the latest board minutes?

- Are any large projects approved, bid out, or already underway?

- Does the building have unresolved permits or violations?

- How much of the monthly fee goes toward reserves?

- Has the seller confirmed whether any assessment balance remains on the unit?

- Are there insurance, maintenance, or litigation issues that could affect future costs?

- Would a lender or insurer view the building as higher risk?

South Florida Lessons After Champlain Towers

The aftermath of Champlain Towers South changed how many buyers look at condo ownership in South Florida. It made building condition, reserve planning, and inspection records impossible to ignore. In coastal markets, structural issues are not just a maintenance topic — they are part of the price of ownership.

That is why Miami-Dade, Broward, and Palm Beach buyers should look beyond the listing photos and into the documents. For investors, special assessments can compress cash flow. For sellers, they can affect buyer demand. For primary-home buyers, they can change whether the unit truly fits the monthly budget.

How Buyers, Sellers, and Investors Should Think About Risk

- Buyers: Focus on reserves, minutes, and permit history before making an offer.

- Sellers: Disclose assessment issues early and be prepared for negotiation.

- Investors: Model the possibility of a large assessment before relying on rental income.

FAQ: Florida Condo Special Assessment 2026

What is the new condo law in Florida 2026?

Florida’s post-Champlain Towers condo safety framework, including SB 4-D, requires structural integrity reserve studies for certain buildings and puts more attention on reserve planning, building condition, and long-term funding.

How to avoid condo special assessment?

You cannot guarantee that a condo will never have a special assessment, but you can reduce the risk by buying a building with a current reserve study, healthy reserves, clear board minutes, documented maintenance, and clean permit and violation history.

Can I sell my condo with a special assessment?

Yes, but the assessment should be disclosed and it can affect your price, timing, and contract terms. In many cases, the seller and buyer negotiate who pays it at closing, so have the estoppel and contract reviewed carefully.

What is the 5 year rule for HOA in Florida?

There is not a single universal 5 year rule in this condo assessment guide. The practical approach is to review at least 5 years of budgets, board minutes, reserve information, and assessment history before buying so you can spot patterns early.

If you are evaluating a South Florida condo and want a cleaner way to check the building before you commit, start with Broker One. Use the available neighborhood data, permit history, and violation information to make a smarter offer and reduce surprise costs.