Average HOA Fees in Miami Condos: Complete Breakdown by Area (2026)

If you’re searching for hoa fees miami condos average, the most useful answer is not a single number — it’s a breakdown by neighborhood, building type, and what the monthly fee actually covers. In South Florida, condo dues can look similar on paper but feel very different once you compare insurance, reserves, amenities, staffing, and the likelihood of future assessments.

April 2026 Data Refresh — What's Changed Since We First Wrote This

This guide was first published in 2024. Since then three things have rewritten the Miami condo HOA picture: SB 4-D milestone inspections hit the December 2024 deadline, reserve studies produced the first wave of large special assessments, and insurance costs became a permanent new line item in every association budget. Below is what our live MLS analysis of 9,372 active Miami-area condo listings shows as of April 2026, plus what it means for anyone buying or selling a Miami condo right now.

Florida Senate Bill 4-D — passed in response to the Champlain Towers South collapse — required buildings 3+ stories to complete milestone structural inspections by December 31, 2024, and to fund reserves based on a Structural Integrity Reserve Study (SIRS). In 2024 this was theoretical; in 2026 it's directly in your HOA bill. The median Miami-area condo HOA has risen approximately 40-55% since 2020, and the increase is not uniform — it's concentrated in older buildings where reserve funding was historically under-capitalized. Our condo inspection law guide explains the legal timeline; this section shows what it did to the numbers.

HOA by Building Era — Older Buildings Paid the Price

The cleanest view of the SB 4-D impact is to group HOA by the year the building was constructed. The 1980s-1990s era was built on thin reserves and has taken the biggest hit in percentage terms. Buildings from 2010 onward were constructed under modern codes and have the highest absolute HOAs but stable trajectories.

Building Era

Median HOA (Apr 2026)

Average HOA

Avg Days on Market

Active Listings

Pre-1980

$825

$992

164

3,621

1980-1999

$1,074

$1,367

138

1,618

2000-2009

$1,387

$1,769

170

2,403

2010-2019

$1,580

$2,233

193

1,318

2020 and newer

$1,514

$2,273

168

882

The surprise is the 2010-2019 cohort: despite being built under modern codes, these buildings are now sitting on the market longest (193 average days). The reason is math — buyers running the numbers on a $1,580/mo HOA plus mortgage plus insurance plus taxes decide it's beyond their monthly threshold even at a fair price. These are the buildings where price discovery is most active right now.

HOA Tier vs Time to Sell — A Direct Correlation

Across every era, higher HOA fees produce longer days on market. This is the most practical correlation in the Miami condo market right now:

Monthly HOA Range

Avg Days on Market

Active Listings

$100-500

140

1,068

$501-1,000

160

3,369

$1,001-1,500

172

2,519

$1,501-2,500

178

1,953

$2,501-5,000

159

983

$5,000+

185

380

The $2,501-5,000 bucket breaks the pattern slightly — these are mostly Sunny Isles, Bal Harbour, and Brickell luxury towers where the qualifying buyer pool is small but decisive. The $5,000+ bucket (380 listings, 185 DOM) is the top of the ultra-luxury tier where HOAs exceed $60K/year. Those units require a buyer who thinks about monthly carrying cost as rounding error — which is a smaller population than it was three years ago.

How This Correlates With the Broader Miami Market

The HOA escalation is one of three forces compressing the Miami condo market in 2026. The other two are insurance (see our rate-by-county breakdown — Miami-Dade averages $12,200/year for a $300K dwelling in 2026) and property taxes (our Florida property tax guide covers why non-homesteaded owners face uncapped annual increases). Together these three line items — HOA + insurance + taxes — now frequently equal or exceed the mortgage payment on Miami condos under $1M. That's a structural change from 2020.

The market's response has been rational and visible:

Newer inventory moves faster at higher absolute HOAs because buyers trust the reserve position. A 2018-built tower at $1,600/mo HOA is easier to underwrite than a 1982 tower at $900/mo where a special assessment could land any month.

Transaction volume is most depressed in the 1985-2005 era — the buildings hitting the 25-year SB 4-D reserve-study threshold right now. Sellers are discounting 15-25% versus 2022 peak to move units.

New construction continues to absorb luxury demand — the Acqualina, Aston Martin, Bentley Residences tier at $2K-5K+ HOA still moves, because buyers at that price point run the HOA math differently.

With that 2026 context in place, the original guide below walks through what HOA fees cover, how to evaluate whether a specific building's fees are reasonable, and what red flags to watch for in the association budget.

This guide is built for buyers, sellers, and investors across Miami-Dade, Broward, and Palm Beach. Use it to compare buildings more intelligently, then check live condo listings at Broker One and neighborhood data at brokerone.io/neighborhoods.

Building type

Is often the biggest driver of monthly dues

Insurance + reserves

Are core cost components in coastal condo budgets

Special assessments

Are separate from regular monthly fees

DTI impact

Lenders count HOA dues in mortgage qualification

A lower monthly HOA fee is not automatically better. In Miami condos, the real question is whether the association is properly funded for insurance, maintenance, reserves, and future repairs.

Average HOA Fees in Miami Condos: What Really Changes by Area

Across Miami and the surrounding South Florida market, HOA fees tend to move with the same few variables: waterfront exposure, building age, staffing, amenity level, and reserve strength. That’s why a simple citywide average can be misleading. A full-service tower in a prime urban or beachfront setting is not comparable to a smaller, older building with limited amenities.

For a practical search strategy, compare condos by neighborhood and building profile rather than by price alone. If you want live neighborhood and building data, start with Broker One’s neighborhood data and then match the association budget to the unit you’re considering.

Often higher when staffing and amenities are extensive

Reserve funding, elevator upkeep, and any pending assessments

Edgewater / Arts & Entertainment District

Newer high-rises and mixed condo inventory

Can be elevated in amenity-rich buildings

What is included in dues and how quickly budgets are rising

Miami Beach

Older coastal buildings plus newer luxury towers

Frequently higher in waterfront or full-service properties

Insurance exposure, capital planning, and structural maintenance

Aventura

Large condo communities and towers

Varies by amenities, age, and included services

Reserve quality and whether utilities are bundled

Sunny Isles Beach

Luxury-oriented coastal towers

Often driven up by service level and oceanfront maintenance

Budget transparency and any history of special assessments

Fort Lauderdale Beach / Las Olas area

Mid-rise and high-rise coastal condos

Can range widely depending on building age and amenities

Recent repairs, reserve contributions, and insurance costs

Boca Raton

Coastal and inland condo stock

Often tied to service level and building condition

How the association handles maintenance and future work

West Palm Beach

Urban condo options with a mix of building types

Depends heavily on amenities and age of the property

Operating budget, reserves, and documented repair plans

Pro tip: Two condos in the same neighborhood can have very different dues if one has front desk staffing, valet, pools, fitness spaces, elevators, or bundled utilities. Compare building-by-building, not just area-by-area.

What HOA Fees Usually Include in a Miami Condo

In Miami condos, the monthly association fee is often more than just a line item. It typically supports the building’s day-to-day operation and long-term upkeep. The exact mix varies by property, but many budgets include a combination of insurance, maintenance, reserves, and amenities.

Insurance for common elements and shared areas of the building.

Maintenance and repairs for lobbies, hallways, elevators, roofs, exteriors, and other shared systems.

Reserve contributions for future major repairs and capital projects.

Amenities such as pools, fitness centers, club spaces, and common lounges when the building offers them.

Security and staffing when a property maintains front desk, patrol, or controlled access services.

Landscaping and common-area cleaning for exterior and shared indoor spaces.

When fees are higher, ask what you are actually getting. A well-run building may justify stronger dues if the budget is funding insurance, staffing, maintenance, and reserves instead of deferring work.

Warning: A fee that looks “cheap” can be a problem if the budget is underfunded. Low dues can sometimes mean weak reserves, deferred maintenance, or a higher chance of special assessments later.

Luxury vs. Mid-Range vs. Affordable Condo Buildings

One of the easiest ways to understand the hoa fees miami condos average conversation is to compare the building itself. In South Florida, monthly dues usually rise as the service level rises. That doesn’t automatically mean luxury buildings are “too expensive”; it means the association is funding a larger operating footprint.

Building Type

Typical Features

Fee Tendency

Best Fit For

Luxury high-rise

Extensive amenities, full staffing, controlled access, multiple common spaces

Usually higher

Buyers who value service, convenience, and building experience

Mid-range condo

Moderate amenity package, less staffing, standard common areas

Typically moderate

Buyers balancing monthly cost with comfort and location

Affordable or older building

Limited amenities, simpler common areas, smaller staff footprint

Often lower, but not always

Buyers focused on monthly affordability and fewer frills

Boutique low-rise

Smaller scale, fewer units, fewer shared services

Can be efficient if reserves are healthy

Buyers who want a quieter building with less overhead

For investors, the key question is not just whether dues are high or low, but whether the building’s expense structure matches the rent potential and the risk of future repairs. A low monthly fee can be appealing, but only if the association’s finances are solid and the building is not pushing costs into the future.

How HOA Fees Change Over Time

Condo dues rarely stay flat forever. In Miami and across coastal Florida, association budgets can change when insurance costs shift, when major systems age, or when the board needs to increase reserves. Buildings with older mechanical systems or heavy amenity loads may need more frequent budget adjustments than simpler properties.

Insurance renewals can push budgets higher when coverage costs change.

Maintenance backlogs force associations to spend more on repairs and upkeep.

Reserve funding changes can increase dues when the building needs to save for future capital work.

Capital projects such as roof, elevator, façade, plumbing, or common-area work can reshape the budget.

Operational changes such as staffing, security, or amenity upkeep can also raise costs.

Buyer takeaway: If a building’s dues have been stable for a long time, that is not always a good sign. Stability can be healthy, but it can also signal that the association has been delaying necessary increases.

Special Assessments vs. Monthly HOA Fees

Monthly HOA fees are the regular operating charge. Special assessments are separate charges used when the association needs extra money for unexpected work, major repairs, or projects that are not fully covered by the regular budget and reserves. In other words, special assessments do not replace monthly dues — they sit on top of them.

This distinction matters in South Florida because a building can appear affordable on a monthly basis and still require a substantial extra payment if major work is underway or newly discovered. That is why sellers, buyers, and investors should ask for written documentation about any current or pending assessment before moving forward.

Critical alert: Do not evaluate a condo by monthly dues alone. A building with low fees and a looming assessment can cost more over time than a building with higher but properly funded monthly dues.

Before making an offer, ask these questions:

Is there a current special assessment?

Is the assessment one-time or ongoing?

What project is it funding?

Are reserves being used, or is the association borrowing time with deferred repairs?

Has the board discussed future work in recent meeting materials?

How to Evaluate Whether HOA Fees Are Reasonable

A reasonable HOA fee is one that makes sense for the building’s age, condition, services, and reserve plan. The goal is not to find the lowest number. The goal is to find a building where the fee reflects actual needs and where the association is managing money responsibly.

Compare similar buildings in the same neighborhood and with similar amenities.

Review what is included in the monthly dues so you can compare total value, not just the headline number.

Look at reserves to understand whether the building is funding future repairs.

Check for recent or pending assessments that could change your true monthly cost.

Inspect the building’s condition for visible signs of deferred maintenance.

Ask about insurance and deductibles because these can affect the budget and future dues.

The best dues are the ones that are honest. If a building’s monthly fee covers real operating needs and reserves, buyers usually get more predictability than they would from artificially low dues.

Investor tip: When evaluating cash flow, model the condo using monthly HOA dues, insurance, taxes, and a cushion for future assessments. That gives a more realistic picture than rent alone.

Red Flags in HOA Budgets

Budget review is one of the smartest things a condo buyer can do. In many cases, the red flags show up before the property is purchased if you know what to look for.

Budget red flags to watch for:

Very low or weak reserves relative to the size and age of the building

Repeated special assessments or frequent talk of upcoming assessments

Visible deferred maintenance in common areas

Large budget gaps that are not clearly explained

Unclear insurance planning or inconsistent budget assumptions

Heavy dependence on one-time income instead of stable operating revenue

If you see more than one of these issues, slow down and review the association documents carefully. In condo ownership, the monthly fee is only part of the story. The budget tells you how the building plans to survive the next few years.

How HOA Fees Affect Mortgage Qualification

For financing, lenders typically count the monthly HOA or condo fee as part of your housing expense when they calculate your debt-to-income ratio. That means a higher association fee can reduce the loan amount you qualify for, even if the purchase price itself looks manageable.

This is important for both end users and investors. Buyers can be surprised when a condo with a strong location and attractive amenities still creates a tighter approval because the monthly dues are high. Investors should also remember that a higher fee directly affects monthly cash flow.

Practical advice: Talk to a lender early in the process, especially if you are shopping in a full-service Miami, Broward, or Palm Beach condo building where monthly dues may be a significant part of the payment.

Tips to Reduce Condo Ownership Costs Without Choosing the Wrong Building

You usually can’t force an association fee lower as an individual buyer, but you can make smarter choices that reduce your overall cost of ownership.

Favor buildings with fewer amenities if monthly affordability is your top priority.

Compare what is included so you do not pay separately for services that another building bundles into dues.

Choose a building with healthy reserves to lower the chance of surprise assessments.

Review recent meeting notes and budgets so you understand where the association is headed.

Look at total monthly carrying cost instead of focusing only on the HOA line item.

Ask about future projects before you make an offer.

Best-value strategy: In many South Florida condo markets, the smartest “lower-fee” purchase is not the cheapest dues number. It is the building that balances service, maintenance, and reserve strength without unnecessary overhead.

FAQ: HOA Fees in Miami Condos

What is the average HOA fee in Miami?

There is no single citywide number that works for every Miami condo. The more useful answer is that HOA fees vary significantly based on building type, amenities, age, insurance, reserves, and location. Full-service waterfront towers usually have higher dues than smaller or older low-amenity buildings.

What is a reasonable HOA fee in Florida?

A reasonable HOA fee in Florida is one that matches the property’s actual operating needs and reserve funding plan. In coastal markets like Miami-Dade, Broward, and Palm Beach, a fee may be higher than inland properties because of insurance, maintenance, and building systems. The key is whether the budget is transparent and the building is being maintained properly.

What is a reasonable HOA fee for a condo?

A reasonable condo fee is one that fits the amenity level, building age, staffing, and reserve health of the property. A fee may be low and still be unreasonable if the building is underfunded. A fee may be high and still be reasonable if it supports full-service operations, repairs, and reserves.

Why are HOA fees so high in Miami?

Miami condo fees can be high because many buildings are coastal, amenity-rich, and staff-intensive. Insurance, maintenance, elevators, security, reserves, and major building systems all cost money. In a market with many high-rise and waterfront properties, those costs can add up quickly.

Ready to compare Miami condo HOA fees the right way? Browse listings at Broker One, then use brokerone.io/neighborhoods to review neighborhood and building data before you buy, sell, or invest.

Broker One Research

Data Journalism & Analysis

Broker One Research is the data-journalism arm of Broker One. Every post under this byline is backed by an original SQL analysis across our proprietary datasets: 2M Florida parcels from county appraisers, 4.6M active and historical MLS listings, 6.9M Florida business entities from Sunbiz, FEMA flood zones, building permits, code violations, and Census ACS demographics. We publish our methodology — row counts, filters, date ranges — so readers can evaluate the rigor of every finding. We use median-based metrics rather than means to keep MLS data-entry outliers out of headline numbers. If you're a journalist or researcher who wants to cite our work, email research@mybrokerone.com.

")

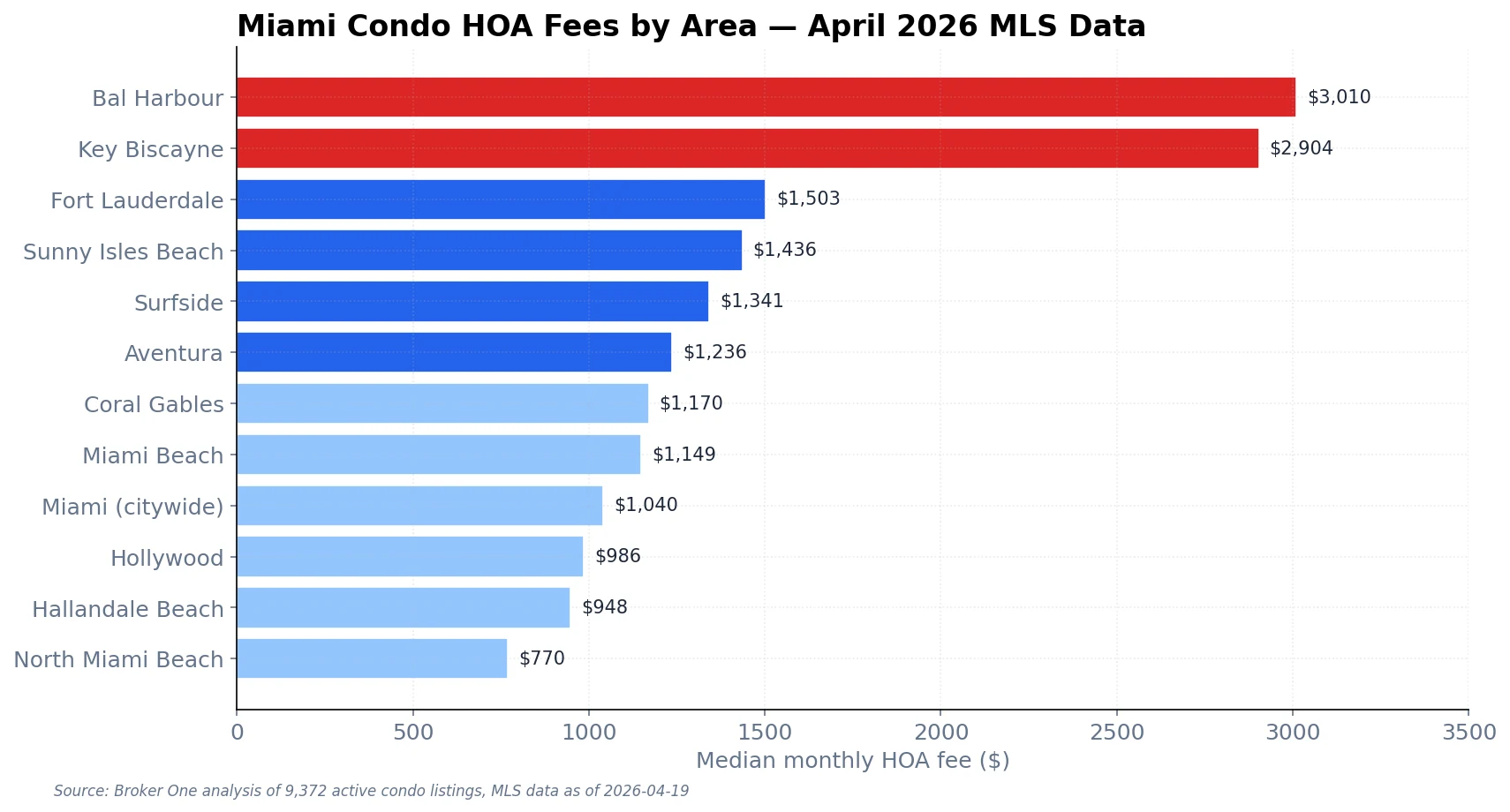

Bal Harbour leads at $3,010,

Bal Harbour leads at $3,010,