The #1 mistake Florida condo buyers make is focusing on the monthly maintenance fee and ignoring the reserve study. In florida condo reserve fund requirements 2026, that can be the difference between a stable building and a surprise special assessment.

If you are buying in Miami-Dade, Broward, or Palm Beach, the post-Surfside rules matter just as much as the view. In 2026, condo due diligence is not only about location and finishes; it is about whether the association has documented inspections, funded reserves, and a realistic repair plan for the building’s structural systems.

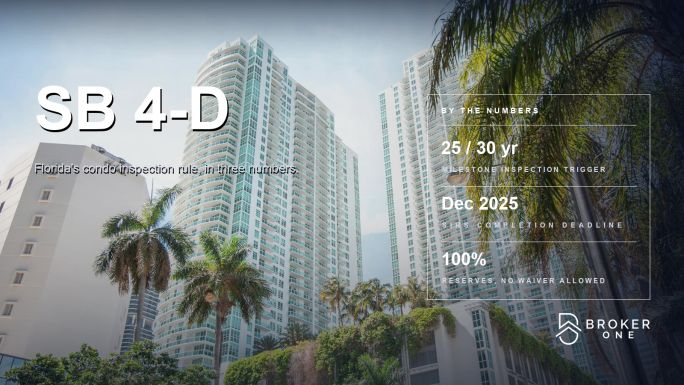

3+

Stories that trigger Florida’s milestone inspection and SIRS rules

30

Years old: standard age threshold for the first milestone inspection

25

Years old if the building is within 3 miles of the coastline

10

Years between required milestone re-inspections and SIRS updates

Buyer warning: A low fee does not mean a safe deal. If the reserve study shows weak funding for structural items, you may inherit delayed repairs, a special assessment, or financing trouble later.

Key takeaway: In Florida condo due diligence, the reserve study is as important as the floor plan. If the building’s long-term repair plan is weak, the monthly fee is not a bargain.

Why Florida tightened condo reserve rules after Champlain Towers South

Florida’s current reserve and inspection framework is part of the post-Surfside safety response that followed the Champlain Towers South collapse. The core idea is simple: buildings that are three stories or more should not wait until a major problem becomes visible before documenting their condition and funding repairs.

That matters in South Florida more than most places because coastal humidity, salt air, and hurricane exposure can accelerate wear on concrete, waterproofing, roofs, windows, balconies, and other structural systems. Buyers should assume the association’s documents matter just as much as the MLS listing.

Buyer protection: If the association cannot show current inspection and reserve documents, treat that as a safety and financing risk, not a paperwork nuisance.

What the Florida condo reserve rules mean in 2026

New SB 4-D reserve requirements buyers should understand

SB 4-D created the modern condo safety framework that buyers still deal with in 2026. For applicable buildings, the association must complete a Structural Integrity Reserve Study, often called a SIRS, and use it to guide reserve funding for critical components.

The key change for buyers is that reserve funding is no longer something you can dismiss as a board preference. For SIRS items, the association is expected to plan for future replacement and funding instead of hoping the issue can be postponed.

- Applies to buildings that are three stories or more.

- Milestone inspections are tied to building age.

- SIRS focuses on structural and safety-related components.

- Reserve funding for SIRS items is mandatory and cannot be waived by owner vote.

What must be fully funded

When a reserve study identifies structural integrity items, those items must be funded through the association’s budget. Buyers should look for reserve planning on the components that affect building safety and major capital replacement.

- Roof

- Structure, including load-bearing walls and primary structural members

- Floor and foundation

- Fireproofing and fire protection systems

- Plumbing

- Electrical systems

- Waterproofing and exterior painting

- Windows and exterior doors

If a building is carrying deferred maintenance on any of these items, the buyer should ask how the board plans to pay for it. “We will deal with it later” is not a financial plan.

Legal requirement: Do not assume the board can waive structural reserve funding just because owners prefer a lower fee. For SIRS items, the reserve obligation follows the law and the study, not the marketing brochure.

| Rule |

Who it affects |

Timing / trigger |

What buyers should request |

| Milestone inspection |

Condos of 3+ stories |

At 30 years old, or 25 years old if within 3 miles of the coastline; every 10 years afterward |

Current inspection report and any repair notices |

| SIRS |

Condos of 3+ stories |

At least every 10 years |

Most recent study and funding schedule |

| Structural reserve funding |

Items listed in the SIRS |

Included in the annual budget |

Reserve line items and board-approved budget |

| Buyer due diligence |

Every condo buyer |

Before offer acceptance and before closing |

Budget, reserve study, minutes, and condo questionnaire |

How to read a reserve study before you buy

A reserve study is not just a checklist. It is a financial snapshot of what the building will need to repair or replace, when it will likely need it, and how the association plans to pay for it. The best buyers read it line by line.

-

Confirm that the study is current.

Ask when it was completed and whether it has been updated since the last major repair, inspection, or budget cycle.

-

Match the study to the building age and trigger.

Make sure the condo is actually subject to the milestone and SIRS rules. A three-story building in coastal South Florida can hit the threshold sooner than buyers expect.

-

Look for the components listed in the study.

Roof, structure, waterproofing, electrical, plumbing, fire protection, windows, and exterior doors should be addressed clearly.

-

Check the remaining useful life assumptions.

If the study says a component has a long life left but visible wear is obvious, ask for the engineering basis behind that assumption.

-

Compare the funding plan to the annual budget.

A reserve study that calls for funding is not enough if the budget does not actually allocate money to those accounts.

-

Cross-check the study against board minutes and assessment history.

Repeated discussion of leaks, concrete repairs, or assessments is a clue that the written budget may not tell the whole story.

Money-saving tip: Ask for the actual reserve study PDF, not a summary from the seller. Then compare it with the condo questionnaire and the most recent approved budget before you make your offer.

Red flags in reserve reports

Red flags: A reserve report can look official and still hide risk. If the report is missing major components, uses vague assumptions, or conflicts with the board’s own records, treat it as a warning sign.

- The SIRS is missing or clearly outdated.

- The study does not list all of the major structural components.

- The reserve budget is far lighter than the study suggests it should be.

- Deferred maintenance is mentioned, but there is no repair timeline.

- Special assessments have already been used, or are being discussed, to cover basic capital needs.

- Board minutes mention repair urgency that does not appear in the reserve schedule.

- The association’s financial documents do not match what the seller or listing agent says.

For buyers, the biggest mistake is thinking a “bad” reserve report only matters to the board. It also affects resale value, lender comfort, and your own monthly carrying costs after closing.

Financial reality: If reserves are underfunded, the shortfall usually does not disappear. It tends to show up later as delayed work, higher dues, or a special assessment.

What happens if the condo is underfunded?

When reserves are short, the association has limited choices. It can defer work, reduce the scope of repairs, raise monthly dues, or levy a special assessment. None of those outcomes are ideal for a buyer who expected a predictable monthly cost.

Underfunding can also create financing friction. Lenders reviewing a condo project want to know whether the building is financially stable and whether major repairs are being addressed responsibly. A weak reserve position can slow down the file or make the project less attractive to conventional financing.

| Reserve position |

What it may mean |

Buyer impact |

| Fully funded |

Budget and reserve study are aligned |

Lower risk of surprise assessments and better lender confidence |

| Partially funded |

Some planned repairs may be pushed or phased |

More due diligence needed before offering |

| Underfunded |

Association may need assessments or emergency funding |

Higher carrying-cost risk and possible financing delays |

Why this matters for conventional financing

If the association does not have enough reserve funds to satisfy a lender’s condo project review, the buyer may not be able to close with a conventional loan on Fannie Mae terms. That does not automatically kill every deal, but it can reduce the pool of eligible lenders and create last-minute surprises.

The fix is simple: get the condo questionnaire, budget, reserve study, and inspection records early enough to solve the problem before your closing clock is running.

South Florida focus: Miami-Dade, Broward, and Palm Beach

Buyers in South Florida should be especially strict about document review because the coastline, humidity, and older condo inventory make inspection and reserve discipline more important. Use local neighborhood research from Broker One here: https://brokerone.io/neighborhoods.

| County |

What to focus on |

Why it matters to buyers |

| Miami-Dade |

Milestone inspection status, SIRS, waterproofing, and reserve funding |

Many buildings are coastal or near-coastal, so the 25-year threshold may apply |

| Broward |

Board minutes, special assessment history, and structural reserve discipline |

Coastal exposure makes inspection timing and repair planning critical |

| Palm Beach |

Current reserve budget, deferred maintenance, and lender-friendly documentation |

Buyers should verify that the association can support long-term ownership costs |

Pro tip: In Miami-Dade, Broward, and Palm Beach, do not judge a building by the lobby alone. Judge it by the reserve study, the inspection record, and how the board handles capital planning.

FAQ: Florida condo reserve fund requirements 2026

What are the new rules for condo reserves in Florida?

For condos that are three stories or more, Florida now requires milestone inspections and a Structural Integrity Reserve Study. The reserve plan must cover the building’s key structural and safety components, and SIRS-related reserve funding cannot be waived by owners.

What is the new condo law in Florida 2026?

There is not one single “2026-only” condo law replacing everything else. In 2026, buyers are still dealing with the post-Surfside law package created by SB 4-D and later amendments, which center on inspections, SIRS, and mandatory reserve funding for structural items.

How often are condo reserve studies required in Florida?

For applicable buildings, the Structural Integrity Reserve Study is required at least every 10 years. Buyers should verify whether the association has a current study on file and whether the annual budget follows it.

What happens when HOA doesn't have enough reserve funds in the account to approve a conventional loan with Fannie Mae?

The lender may not be able to approve the condo project for a conventional Fannie Mae loan. In practice, that can mean financing delays, the need for different loan terms, or a different financing path altogether. Ask for the condo questionnaire and budget early so you can spot the issue before closing.

If you are comparing condos in Miami-Dade, Broward, or Palm Beach, use Broker One for neighborhood research and local condo context: https://mybrokerone.com. Start with the neighborhood pages here: https://brokerone.io/neighborhoods.

- Current SIRS and milestone inspection reports

- Most recent approved budget and reserve schedule

- Board minutes from the last 12 months

- Special assessment history and any pending assessments

- Deferred maintenance notices or repair timelines

- Condo questionnaire and lender review results

- Insurance information and any known claims issues

- Attorney and lender review before removing contingencies

")