Edgewater Miami new construction sells. Worldcenter hotel-condos don't.

Two Miami markets, one vintage, opposite outcomes

After we published the Miami 2026 new-construction pipeline post yesterday, a Reddit commenter on r/REBubble pushed back with a useful framing: "a lot of the units for sale aren't the units that will appeal to the ultra-luxury buyer." Trophy units clear; mid-stack sits. We dug into our MLS data to test the within-building absorption pattern. The data validates the spirit of the comment but reframes the actual axis of the stall.

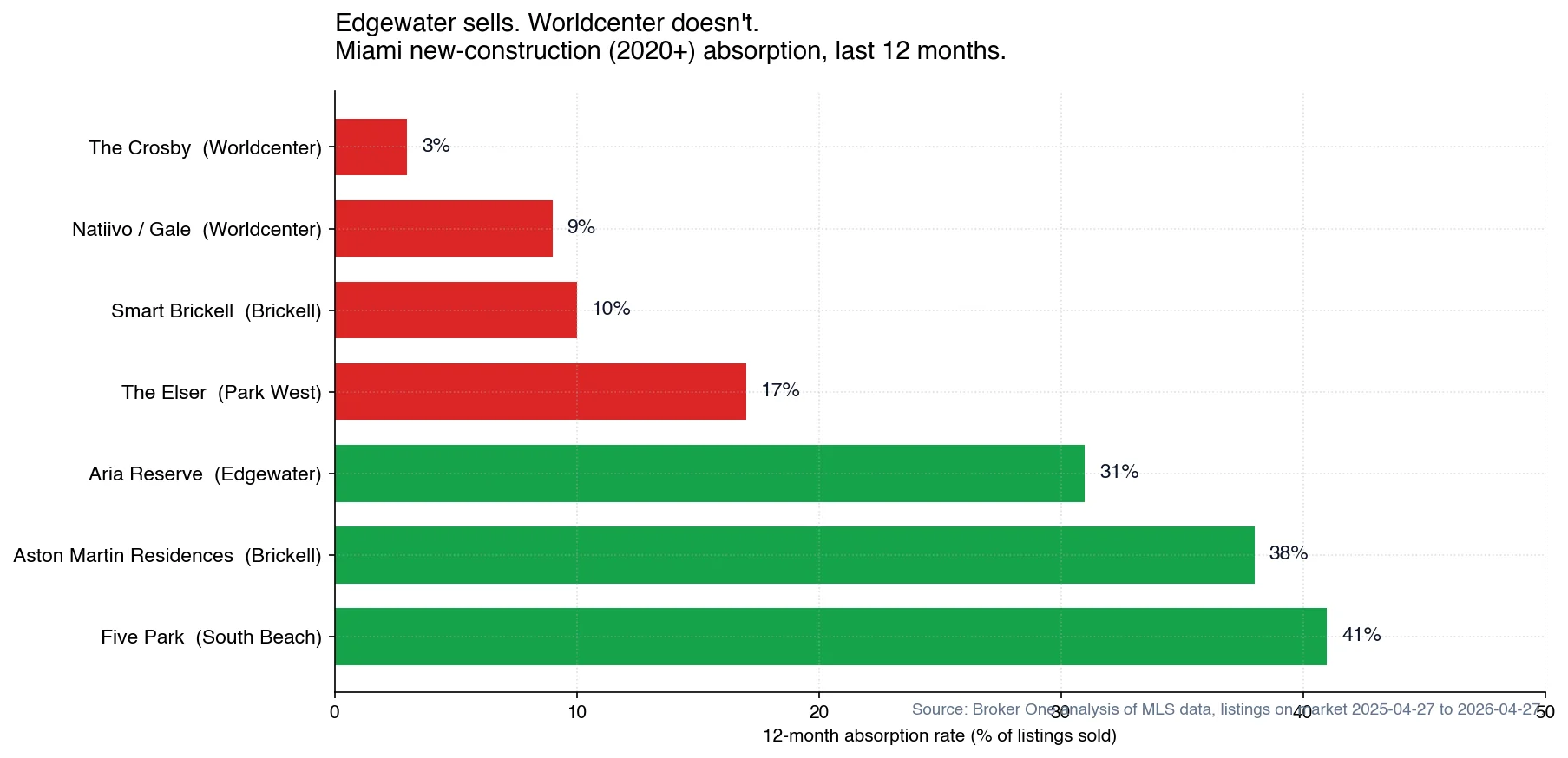

The pattern isn't trophy-vs-stack. It's studio + 1BR investor product vs. 2BR+ family product, concentrated in a specific window of 2024-2026 deliveries in Downtown Miami's Worldcenter cluster. Towers built for short-term-rental investors are clearing at 3-17%. Towers built for end-user families are clearing at 31-41%.

Last-12-month absorption rate by tower for 2020+ Miami new-construction inventory. Red is the studio-investor cluster; green is the family-condo cluster.

The split is geographic too

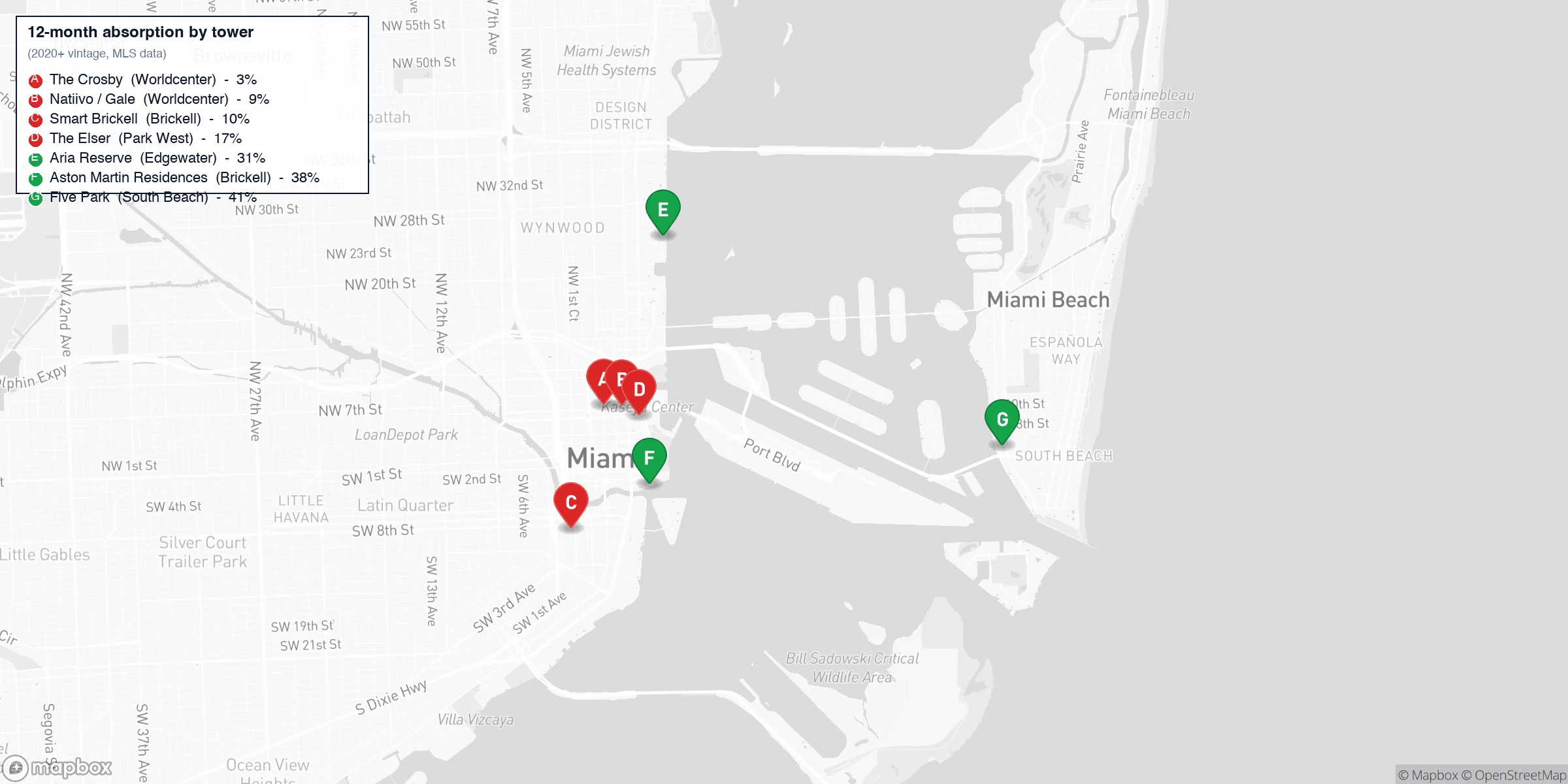

Map the seven towers and the pattern hardens. Worldcenter and southern Brickell carry the entire stall. Edgewater and South Beach carry the clearance. The four red pins all sit within a single half-mile radius around the Miami Worldcenter master-plan; the three green pins sit on water-frontage corridors with established residential character.

The stall is geographic. Four red pins inside the Worldcenter half-mile, three green pins on established waterfront corridors.

Bedroom count is the strongest predictor we found

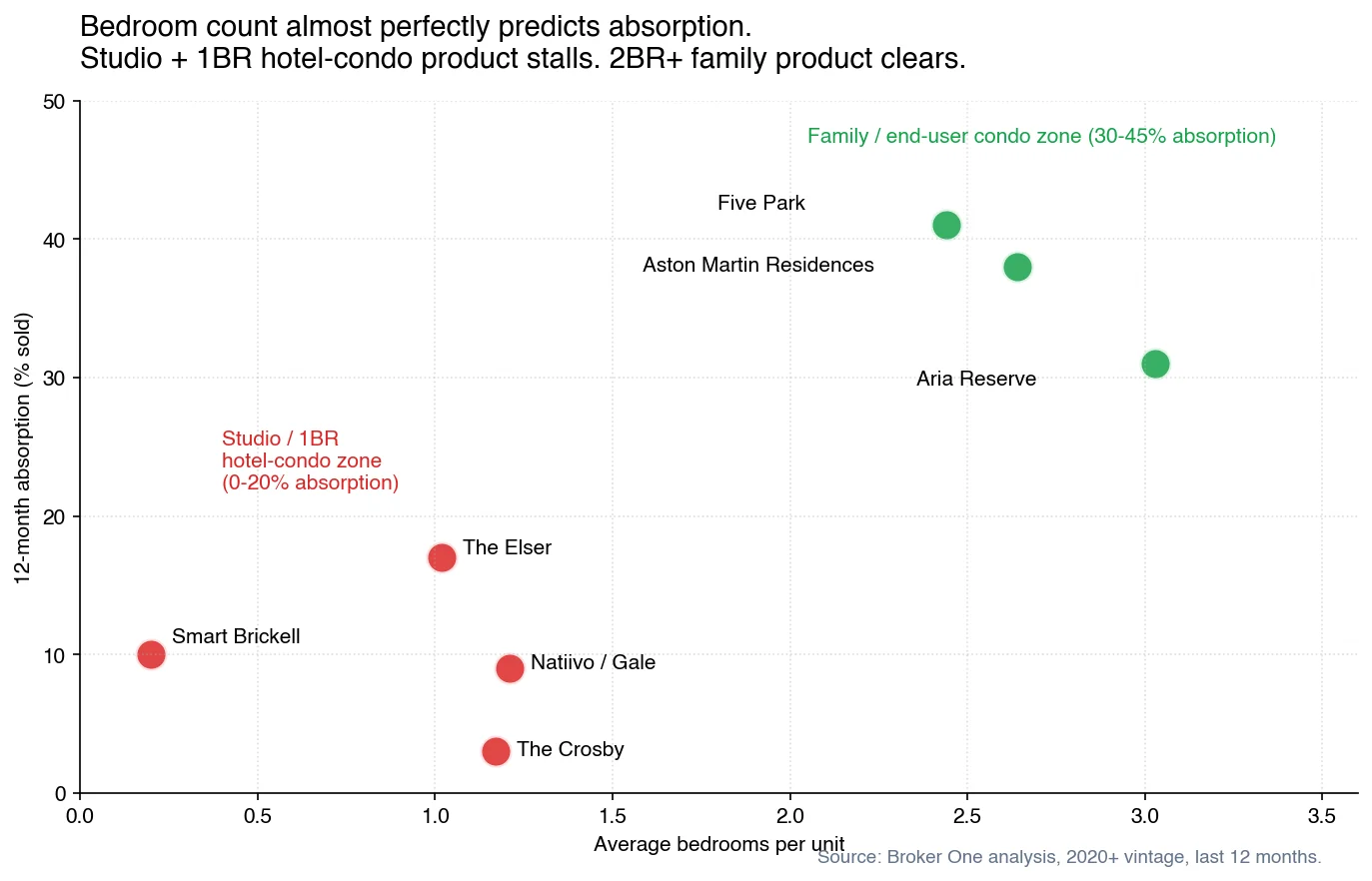

Plot bedrooms against absorption and the relationship is almost a clean line. Every tower under 1.5 average bedrooms sits at 0-20% absorption. Every tower at 2.4+ bedrooms clears at 30%+. There's no overlap between the two clusters in our cohort.

Bedroom count predicts absorption with almost no overlap. The studio-investor product was built for a short-term-rental thesis the market is no longer underwriting.

The four red towers are all hotel-residence or hotel-condo concepts pitched at investors who would Airbnb the unit. The Crosby and Natiivo are programmed at the Gale Hotel; Smart Brickell pitches itself directly to short-term-rental operators; The Elser runs as a hotel-residence inside the Elser Hotel. Average bedroom count under 1.25 isn't a coincidence. It's the product spec for a rental-yield buyer, not a household.

Three things changed against that thesis between 2023 and 2026:

Mortgage rates compressed STR cash-on-cash math. A 2024-2026 buyer financing 70% LTV at 6.5%+ on a $700K studio gets crushed by the debt service, the HOA, and the property tax stack against the realistic Airbnb-net annual revenue. The math that worked at 3.5% rates doesn't work at 6.5%.

Miami-Dade and Miami Beach tightened short-term-rental enforcement. Buildings are quieter, fines are higher, hosts are less protected. The product-market fit for "buy a Downtown studio and rent it nightly" got worse, not better.

The post-pandemic STR investor cohort already bought. Anyone who was going to make this trade made it in 2021-2023. The current pool of buyers is thinner, more skeptical, and pricier to convince.

HOA-per-square-foot alone doesn't explain the stall

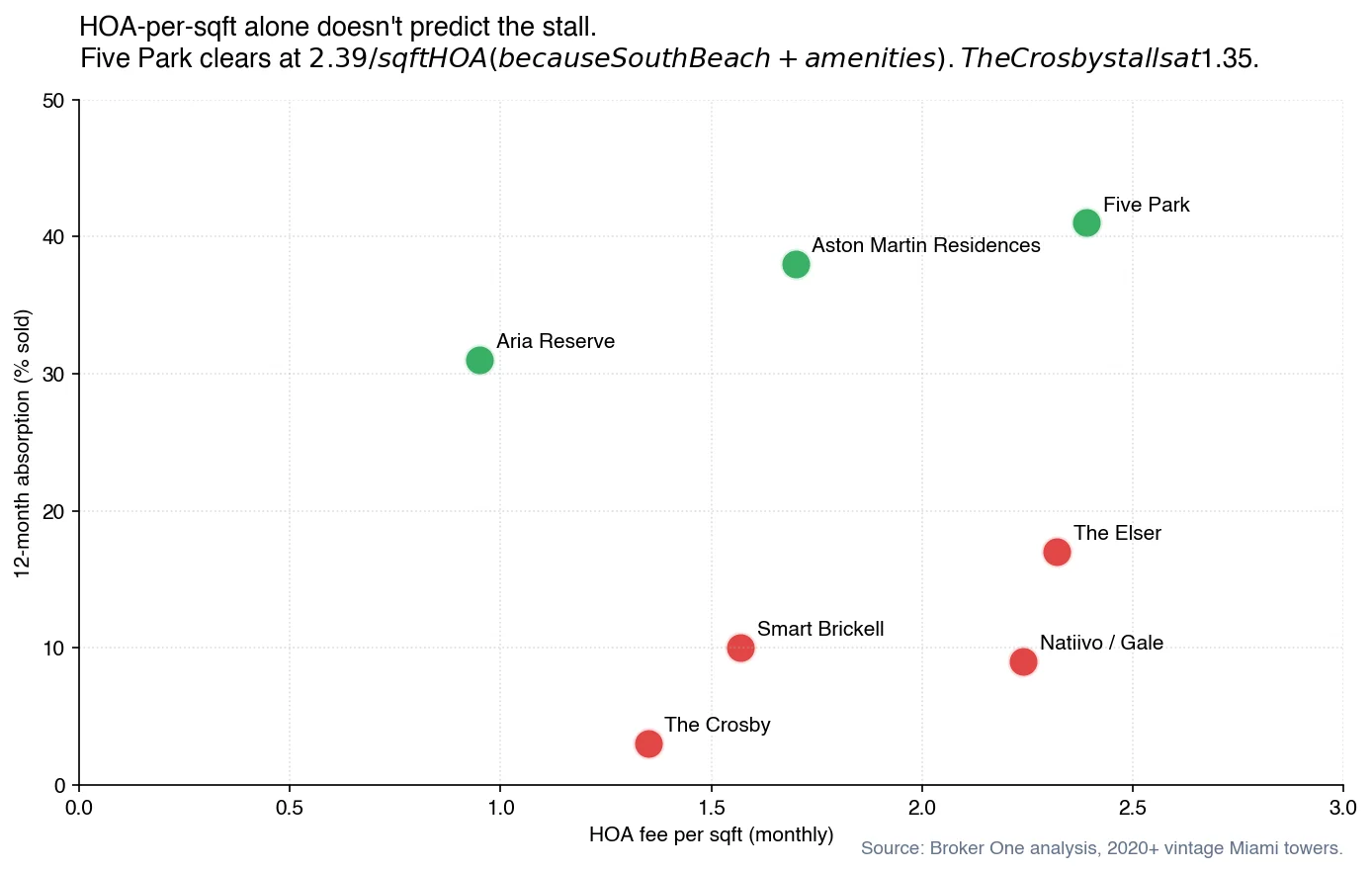

The intuitive explanation, that stallers carry crushing HOA fees, only partially holds. Five Park sells at the highest HOA-per-sqft in the cohort ($2.39) and clears at 41% because South Beach demand validates the cost. The Crosby carries a relatively modest $1.35 HOA-per-sqft and still sits at 3% absorption.

HOA-per-sqft alone doesn't predict absorption. Five Park clears at the highest HOA in the cohort. The Crosby stalls at the second-lowest.

What does seem to matter: the ratio of amenity count to HOA cost, and whether the location-and-product combination has a buyer pool that values that amenity stack. Aria Reserve carries the lowest HOA-per-sqft in the cohort ($0.95) and the highest amenity count (~12 distinct features in the MLS data). That combination clears at 31% on a 3.0-bedroom average, which is the bedroom-and-amenity profile that defines an end-user condo rather than an investor unit.

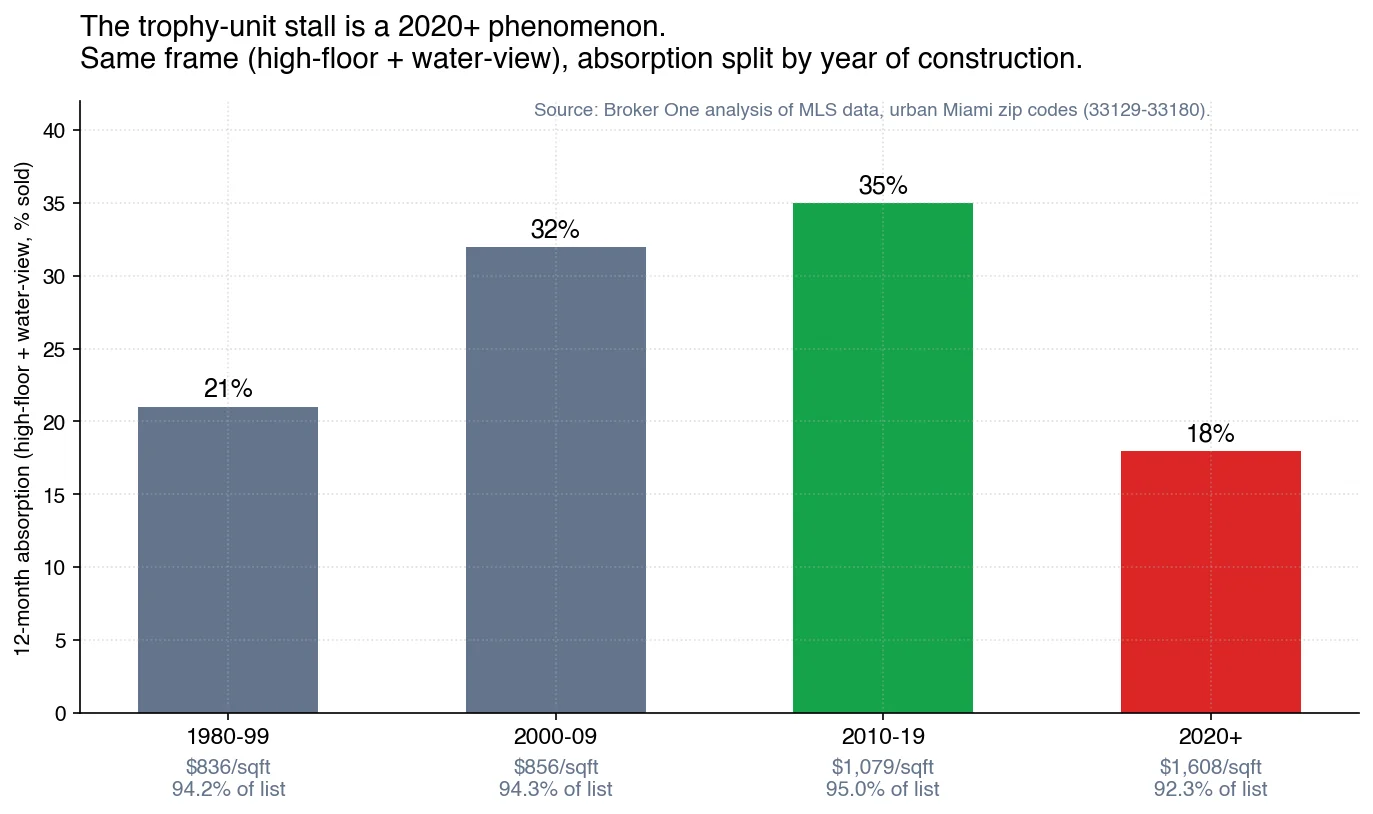

This is a 2020+ phenomenon

The cleanest framing of the stall: it's this vintage. Take the same simple unit definition (high-floor + water-view residence in urban Miami) and split absorption across construction eras. The 2020+ cohort sits at 18% absorption with 92.3% close-of-list, while the 2010-19 cohort clears at 35% with 95.0% close-of-list, even though the 2020+ product is asking 49% more per square foot.

The same unit frame (high-floor + water-view) clears at half the rate in 2020+ buildings versus 2010-19, despite asking 49% more per sqft.

Buyers who want a 2010-19 trophy unit can get it at $1,079/sqft today with a 5% negotiation. The same trophy frame in 2020+ construction asks $1,608/sqft, takes 30 days longer to sell, and the seller still gives up 8% off list. Pricing power has shifted to buyers in the new-construction cohort, while the prior decade's stock is in equilibrium.

What buyers should do with this

If you're shopping urban-Miami new construction in the 2020+ cohort, the data points to specific tactics:

If you want a studio or 1BR in Worldcenter or Park West, you have material negotiation room. The Crosby's listings on average close at 100% of list (small sample) but only 3% have closed at all in 12 months. Sellers are holding a price they can't get filled. List price minus 8-10% is a defensible opening offer at the 0-15% absorption towers.

If you want a 2BR+ family unit in Edgewater, Brickell, or South Beach, you're competing in a 30-40% absorption market. Negotiation is more like 4-6% off list, units move in under 100 days, and sellers can wait you out.

If you're buying for STR yield specifically, model the gross at current Miami short-term rental rates and current building HOA. Net out at the financing cost you actually qualify for, not the cost a 2021 pre-construction buyer was modeling.

What sellers should do

If you're holding a 2020+ Worldcenter studio, the comparable data isn't in your favor. Either reprice to the cohort's actual close $/sqft (which is below the original developer pricing for most 2024-delivery hotel-residences), or pivot to long-term unfurnished rental and wait for the 2027-2028 absorption window when the city's STR enforcement and rate environment may shift again.

If you're holding a 2BR+ in Edgewater or South Beach, the data says hold ground on price and let DOM tick toward 100 days. The 30-40% absorption rate is doing the work for you.

What developers should do

The product spec that worked in 2021-2023 (small studios + 1BR with hotel licensing) has stalled. Developers underwriting new pre-construction in 2026 should size more 2BR+ inventory, calibrate amenity-cost ratios closer to Aria Reserve's, and pick locations with established residential character (Edgewater, South Beach, established Brickell waterfront) over the Worldcenter master-plan, which is producing the worst absorption of any 2020+ cohort in our data.

Methodology

We pulled all listings active or closed in the 12 months ending today across urban Miami zip codes 33129, 33130, 33131, 33132, 33137, 33139, 33140, 33141, 33154, 33160, 33180, and 33009: Brickell, Downtown, Park West, Edgewater, Midtown, South Beach, Mid Beach, Surfside, Bal Harbour, Sunny Isles, Aventura, and Hallandale. We restricted to buildings with YearBuilt >= 2020 and aggregated absorption (sold / total listings), median days-on-market, $/sqft list and close, ratio of close to list, average bedrooms, monthly HOA fee, and amenity count per tower. We resolved towers via tight lat/lng polygons rather than the MLS subdivision_name field, which is heavily fragmented in the source data. Cohort is restricted to listings with living area > 200 sqft and list price > $100,000.

This is an MLS-data analysis. It does not include off-market trades, all-cash flips below the public listing window, or listings actively withheld by the developer. The 2020+ pipeline cohort is partially still under construction or in initial sell-down. Early absorption rates here may improve over time, but the cross-vintage comparison shows the 2020+ profile is materially weaker than 2010-19 was at the same point in its lifecycle.

Where this goes next

We're building floor-and-view filters into the Broker One property search so readers can replicate this analysis on the live MLS data themselves: pick any building, set a tier (studio / 1BR / 2BR+ family / penthouse) and a view tier (water / no-water), and see what's actually moving. We'll cross-link from this post when it ships. In the meantime, the per-tower data is current as of today; the methodology is reproducible from the public MLS feeds.

Broker One Research is the data-journalism arm of Broker One. Every post under this byline is backed by an original SQL analysis across our proprietary datasets: 2M Florida parcels from county appraisers, 4.6M active and historical MLS listings, 6.9M Florida business entities from Sunbiz, FEMA flood zones, building permits, code violations, and Census ACS demographics. We publish our methodology — row counts, filters, date ranges — so readers can evaluate the rigor of every finding. We use median-based metrics rather than means to keep MLS data-entry outliers out of headline numbers. If you're a journalist or researcher who wants to cite our work, email research@mybrokerone.com.