Florida Home Insurance 2026: Rate-by-County Breakdown

Florida home insurance is finally turning a corner. After four years of runaway premiums, carrier insolvencies, and Citizens policy counts climbing past 1.4 million, the state is entering 2026 with its first broad rate cuts since 2019. But the relief is deeply uneven — what you pay depends less on your ZIP code's median home price than on how far you are from the coast, how old your roof is, and whether your county carries a litigation surcharge baked into carrier filings.

$3,815

Statewide average annual premium (2026, $300K dwelling)

-8.7%

Citizens Insurance avg rate reduction for 2026

9.2x

Ratio of highest to lowest Florida county premium

395,144

Citizens policies in force — down 72% from 2022 peak

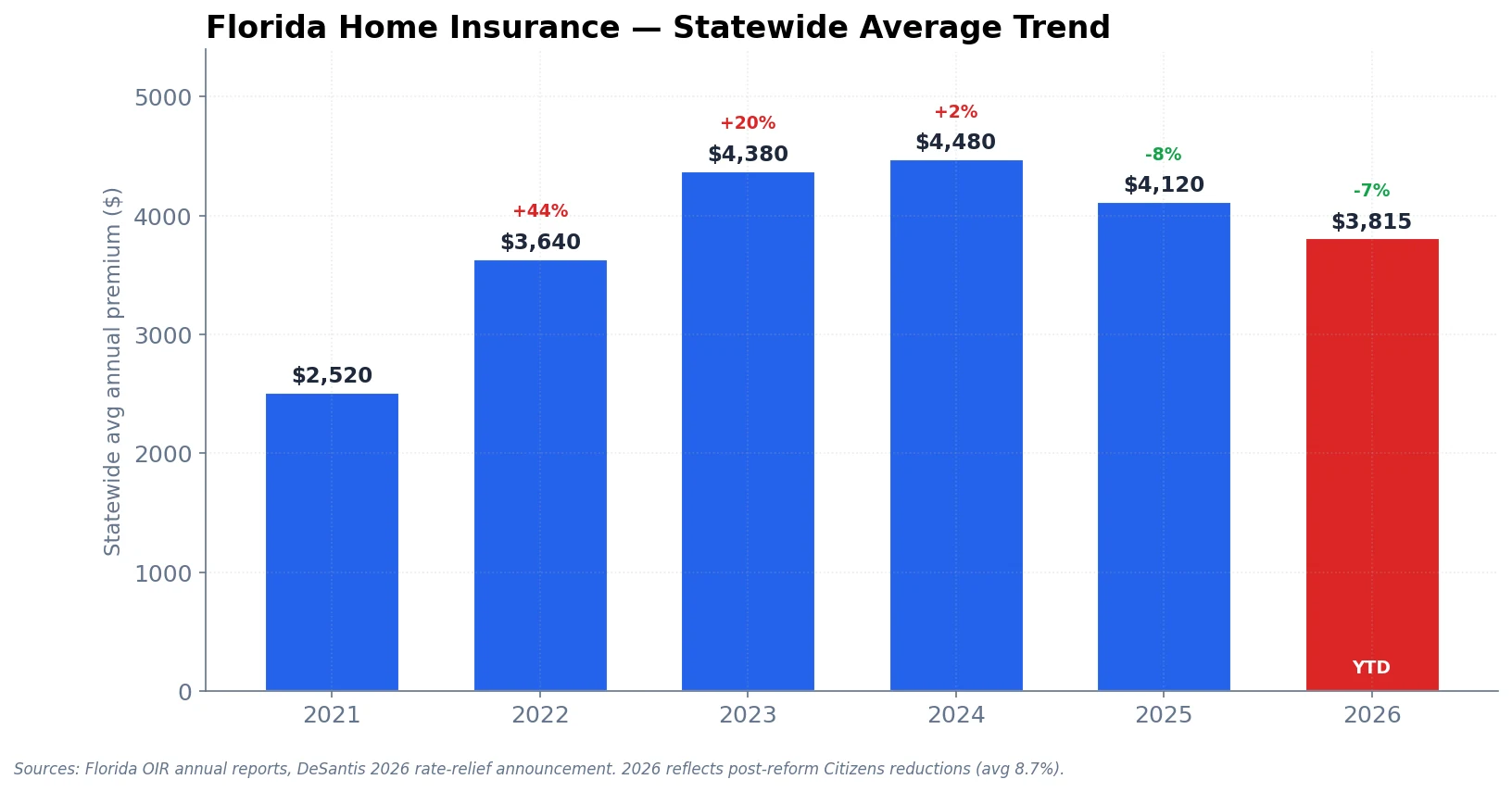

The Statewide Trend — A Real Inflection

From 2021 to 2024 Florida homeowners lived through the sharpest insurance-premium escalation in the country. The statewide average climbed from $2,520 to $4,480 — a 78% increase in three years. Carrier insolvencies (Southern Fidelity, FedNat, United Property, Weston, Avatar, UPC) pushed hundreds of thousands of policies into Citizens Property Insurance Corporation, the state-run insurer of last resort. Reinsurance costs tripled. Private carriers that remained hiked rates 25-40% annually.

2025 was the first year that pattern broke. Legislative reforms — elimination of one-way attorney fees, restrictions on assignment-of-benefits claims, stricter roof-age underwriting — filtered through the market. Carriers started returning: Slide, Loggerhead, Monarch National, American Integrity Plus. Citizens began "depopulation" programs moving policies back to private market. The statewide average dipped 8% to $4,120.

2026 is the first real broad rate cut. Governor DeSantis announced a Citizens average reduction of 8.7% statewide in spring 2026. State Farm filed a 10% reduction. USAA 7%. Progressive, GEICO, Allstate each approximately 8%. The statewide 2026 average settles at roughly $3,815 — below 2024 levels but still 51% above 2021.

Florida statewide average home insurance premium, 2021-2026. The 2026 decline reflects Citizens' 8.7% average reduction plus private-carrier filings between -7% and -10%. Source: Florida OIR annual reports, DeSantis 2026 rate-relief announcement.

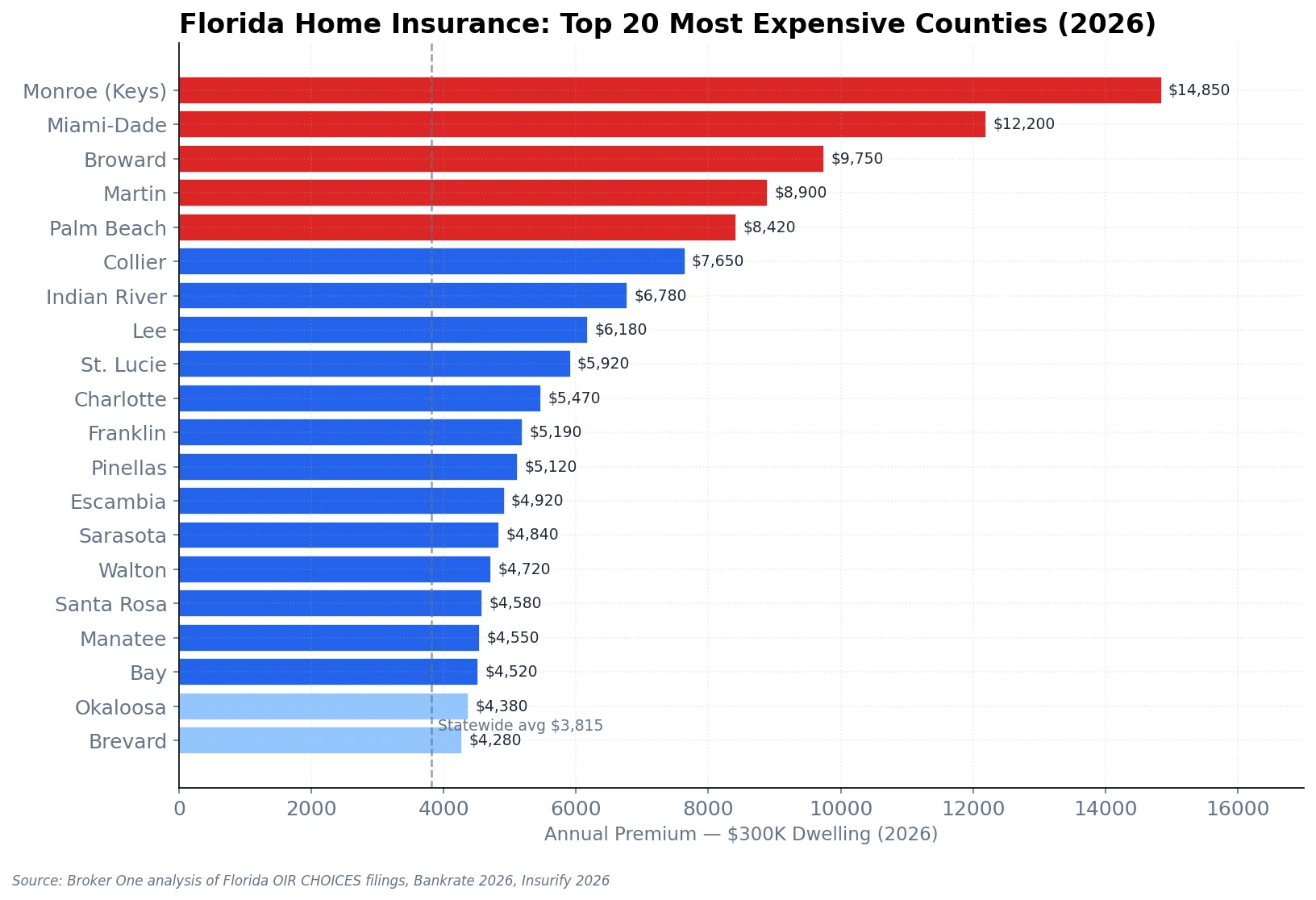

Rate-by-County — Why a 9x Spread Exists

No U.S. state has anything like Florida's geographic rate variance. A single-family $300K dwelling in Sumter County pays $1,620/year. The same home in Monroe County (Keys) pays $14,850. That's a 9.2x spread within a single state, and it tracks almost perfectly with distance from open water and hurricane-loss history.

The table below shows the 20 most expensive counties and the 10 least expensive. Values are 2026 average annual premiums for a $300,000 dwelling coverage single-family policy with $2,500 hurricane deductible.

Top 20 Florida counties by 2026 home insurance premium — $300K dwelling, $2,500 hurricane deductible. Source: Broker One analysis of Florida OIR CHOICES filings, Bankrate 2026, Insurify 2026 data.

The Expensive Tier — Keys, South Florida Coast, Treasure Coast

County

2026 Premium

2025 Premium

YoY Change

Monroe (Keys)

$14,850

$16,200

-8.3%

Miami-Dade

$12,200

$13,630

-10.5%

Broward

$9,750

$11,782

-17.2%

Martin

$8,900

$10,625

-16.2%

Palm Beach

$8,420

$9,105

-7.5%

Collier

$7,650

$8,240

-7.2%

Indian River

$6,780

$7,220

-6.1%

Lee

$6,180

$6,840

-9.6%

St. Lucie

$5,920

$6,340

-6.6%

Charlotte

$5,470

$5,990

-8.7%

Franklin

$5,190

$5,560

-6.7%

Pinellas

$5,120

$5,680

-9.9%

Escambia

$4,920

$5,280

-6.8%

Sarasota

$4,840

$5,310

-8.9%

Walton

$4,720

$5,080

-7.1%

Santa Rosa

$4,580

$4,910

-6.7%

Manatee

$4,550

$5,020

-9.4%

Bay

$4,520

$4,850

-6.8%

Okaloosa

$4,380

$4,670

-6.2%

Brevard

$4,280

$4,580

-6.6%

Broward's 17% cut is the largest in the state by a wide margin — a combination of Citizens depopulation, the 8.7% base reduction, and two private carriers (Loggerhead, American Integrity Plus) aggressively taking policies out of Citizens at below-Citizens rates. Miami-Dade is next at -10.5%. Martin County (Stuart/Jensen Beach) benefits from a roof-age policy change that removed several thousand older homes from high-risk surcharge tiers.

The Affordable Tier — North-Central Inland

County

2026 Premium

Region

Sumter

$1,620

Central inland (The Villages)

Baker

$1,720

North-central inland

Columbia

$1,740

North-central inland

Marion

$1,820

North-central inland

Lake

$1,920

Central inland

Alachua

$1,940

North-central (Gainesville)

Polk

$2,080

Central inland

Seminole

$2,090

Central inland (Orlando metro)

Leon

$2,140

Big Bend (Tallahassee)

Orange

$2,180

Central inland (Orlando)

The cheapest Florida insurance is in Sumter County at $1,620/year. The same coverage on a Miami-Dade coastal home runs $12,200 — and $14,850 in the Keys. Distance from the Gulf or Atlantic is the single biggest driver of your premium.

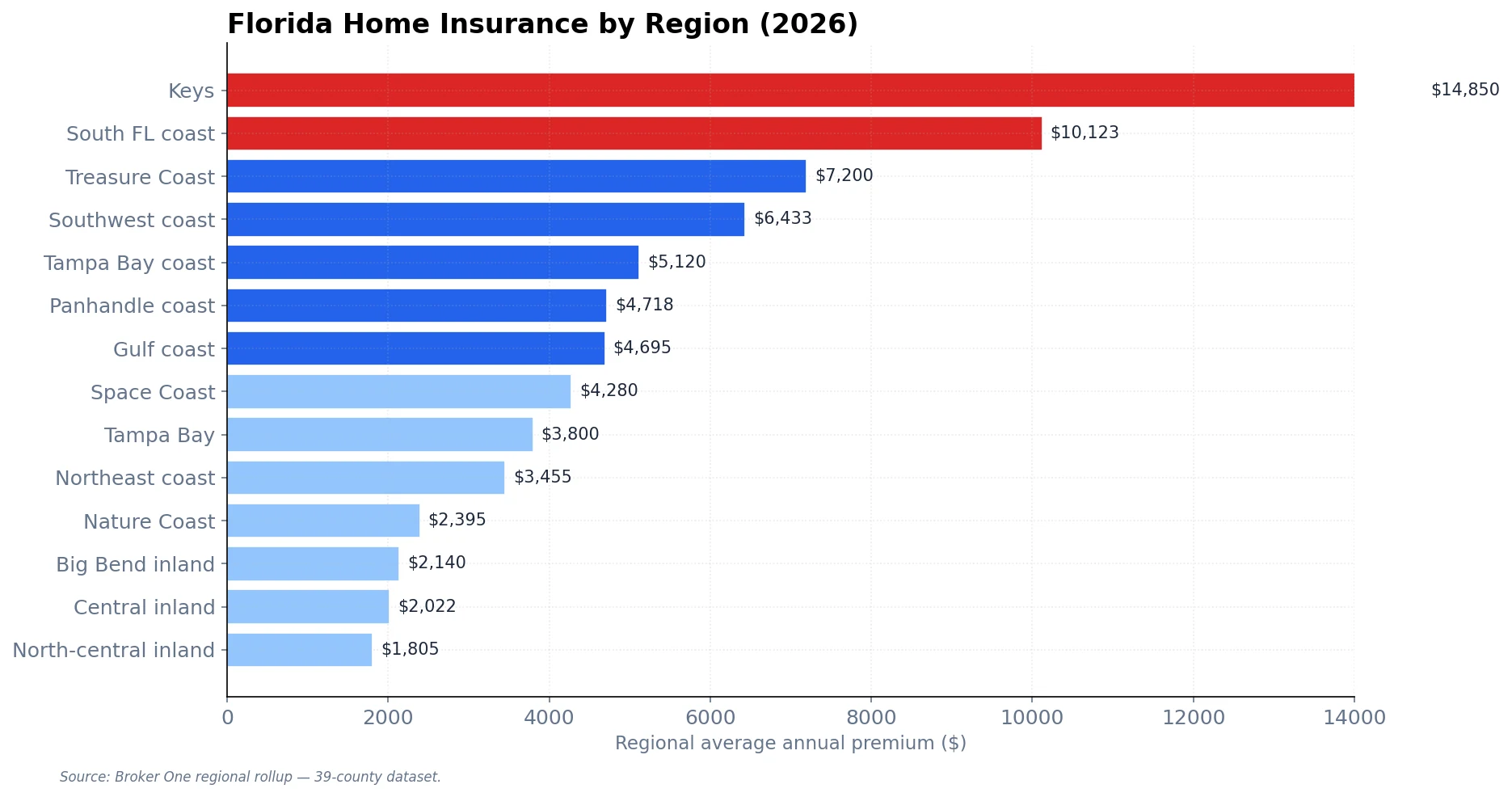

Regional Averages

Florida 2026 home insurance premium by region. Source: Broker One analysis of Florida OIR CHOICES filings, Bankrate 2026, Insurify 2026 data.

Three patterns emerge:

Keys and barrier islands remain a category by themselves. Hurricane surge risk, limited reinsurance appetite, and a small pool of insurable units produce premiums that don't benchmark against anything else in the state.

Southeast metro (Miami-Dade/Broward/Palm Beach) and the Treasure Coast (Martin/Indian River/St. Lucie) are the big-volume high-rate tier. Most Floridians paying $6K-12K live here.

Inland central and north-central counties are dramatically cheaper — often 3-5x less than their coastal counterparts 60 miles away. Orlando metro (Orange/Seminole) at $2,180/$2,090 vs. Brevard (Space Coast) at $4,280 is a good local example of how quickly the coastal surcharge disappears once you move inland.

Why Rates Vary So Much by County

Six factors combine to produce your county's premium:

1. Distance from open water (the dominant factor)

Windstorm reinsurance cost is the single largest component of a Florida premium — often 40-55% of the total. Reinsurance cost scales sharply with proximity to the coastline and is nearly binary between "barrier island" and "mainland." A home in Fort Lauderdale five blocks from the ocean can cost 3x what an identical home in Plantation (8 miles inland) pays.

2. Roof age and material

Roofs older than 15 years frequently trigger surcharges, reduced coverage options, or outright non-renewal. Shingle roofs are surcharged relative to tile or metal. Many carriers now require proof of a wind-mitigation inspection plus a roof certificate confirming remaining useful life before quoting.

3. Hurricane deductible selection

Florida hurricane deductibles are a percentage of dwelling coverage — typically 2%, 5%, or 10%. Choosing a 5% deductible ($15,000 on a $300K home) instead of 2% ($6,000) can cut your premium 15-25%. Most buyers default to 2% without realizing the tradeoff.

4. Flood zone designation (SFHA)

If your property is in a FEMA Special Flood Hazard Area (Zones A or V), flood coverage is separate from your homeowner policy and added via NFIP or private flood. Even outside an SFHA, carriers price wind-driven rain and surge exposure into the main policy.

5. Litigation climate

Pre-reform, Florida accounted for 11% of U.S. homeowner insurance claims but 73% of all insurance litigation nationally. The 2022-2023 reforms reduced this sharply, but carriers still price a "litigation factor" by county — Miami-Dade, Broward, and Palm Beach have historically carried the highest multipliers due to plaintiff-friendly venue selection.

6. Citizens penetration

In areas where Citizens is the dominant carrier, private alternatives are scarcer and more expensive. Citizens' 2026 rate cuts set the benchmark — private carriers in high-Citizens counties must come in at or below Citizens pricing to win business, which is why Broward and Miami-Dade got the largest cuts.

Who's Cutting Rates in 2026

Carrier

2026 Average Change

State Farm Florida

-10.0%

Citizens (Multiperil)

-8.8%

Progressive

-8.5%

GEICO

-8.0%

Allstate

-8.0%

USAA

-7.0%

State Farm's 10% cut is the largest among major carriers and reflects that carrier's aggressive return to the Florida market after pulling back in 2022-2023. USAA's smaller 7% cut reflects its military-exclusive book already being better-selected than the general population.

How to Lower Your Florida Home Insurance Premium

In order of savings impact, the most effective actions are:

Get a wind mitigation inspection (~$150 cost, typically saves $400-1,500/year). This documents features like hurricane shutters, impact-rated windows, a hip roof shape, and roof-deck attachment method — each of which earns a credit.

Raise your hurricane deductible to 5% or 10%. If you have enough savings to absorb $15K-30K in a hurricane, the premium savings stack every year you don't file a claim.

Replace a roof older than 15 years before shopping rates. A new roof often unlocks private-market options that don't exist for older-roof homes.

Bundle with auto. Most major carriers offer 10-15% multi-policy discounts.

Raise your dwelling deductible to $2,500 or $5,000. Only matters for non-hurricane claims but stacks modestly.

Shop every renewal. Unlike most states, Florida's carrier landscape changes substantially year-over-year. A quote that didn't exist in 2024 may be your best option in 2026 (Slide, Loggerhead, Monarch National, American Integrity Plus).

Citizens vs Private Market in 2026

Citizens Property Insurance is the state-backed insurer of last resort. By statute, you can only buy a Citizens policy if no private carrier will offer comparable coverage within 20% of Citizens' rate. In 2022 that meant most South Florida coastal owners defaulted to Citizens because private carriers wouldn't touch them. In 2026 the picture is different — Citizens' policy count is down to 395,144 from a peak of 1.4 million, and most homeowners now have at least one private option.

When Citizens still wins: homes in barrier-island ZIP codes, older roofs with limited private-market interest, prior claim history that eliminates private options, and homes where the private quote is more than 20% above Citizens (the statutory trigger for Citizens eligibility).

When to take a private carrier offer: most mainland coastal and all inland homes. The private market generally offers broader coverage, more flexible deductibles, and — critically — no Citizens assessment risk. After a major hurricane Citizens can assess policyholders retroactively to cover losses; private policies carry no such liability.

The Frequently Asked Questions

Why is Florida home insurance so expensive?

Four reasons: hurricane reinsurance cost, litigation history (pre-2023), older housing stock with aging roofs, and a concentration of high-value coastal properties. Florida represents roughly 11% of U.S. homeowner claims by count but, pre-reform, 73% of U.S. insurance litigation. Reinsurance markets price that risk in.

What's the cheapest home insurance in Florida?

In 2026, Sumter County averages $1,620/year on a $300K dwelling. Other sub-$2,000 counties: Baker, Columbia, Marion, Lake, Alachua. All are north-central inland — 60+ miles from the coast.

Are insurance rates actually going down in 2026?

Yes, for the first time in four years. Citizens is cutting an average 8.7% statewide. State Farm, USAA, GEICO, Allstate, and Progressive all filed rate decreases between 7% and 10%. Broward County is seeing the largest cut at approximately 17% year-over-year.

How much does home insurance cost on a $500,000 house in Florida?

Using 2026 statewide average rates scaled to $500K dwelling, expect roughly $6,358/year statewide. In Miami-Dade that figure rises to approximately $20,333/year. In Sumter or Baker County it's approximately $2,700/year. Your actual quote depends on roof age, deductible selection, and wind mitigation credits.

Do I have to buy flood insurance?

Federally-backed mortgages require flood insurance if the property is in a Special Flood Hazard Area (Zones A or V). Outside SFHA it's optional — but still recommended in most of coastal and low-lying Florida. Private flood carriers (Neptune, TypTap, FloodFlash) now offer more flexible alternatives to NFIP with higher limits.

Should I buy a home with an older roof?

It depends how old. Roofs under 15 years are broadly insurable. Roofs 15-25 years face surcharges and limited carrier options. Roofs older than 25 years are frequently uninsurable on the private market and may force a Citizens policy. Budget for roof replacement in your offer if the existing roof is nearing the 15-year mark.

What's a hurricane deductible?

A separate deductible that applies only to hurricane claims (not other windstorm or non-hurricane claims). It's a percentage of dwelling coverage rather than a fixed dollar amount — typically 2%, 5%, or 10%. On a $300K home, a 2% hurricane deductible is $6,000 out of pocket per event; a 5% is $15,000.

What This Means for Buyers

If you're writing offers in 2026, three practical implications:

Get an insurance quote before your offer is accepted. Not after. Not during inspection. Before — because 2026 rates are unpredictable on a per-property basis and the quote can shift your all-in carrying cost by $5K-15K/year on a South Florida coastal property.

Ask for a wind mitigation report from the seller. Most sellers won't have one. If they do, your quote is faster and more accurate. If they don't, budget $150 and order one before closing.

Read the 4-point inspection carefully. Roof age, electrical panel, plumbing material, and HVAC age are the four pillars that determine whether your home is insurable at standard rates, surcharged rates, or Citizens-only.

For a deeper look at Florida's insurance landscape — the carrier insolvencies, assignment-of-benefits reforms, and what Citizens depopulation actually means for your bill — read our Florida Home Insurance Crisis guide. If you're in the middle of calculating whether a condo is worth its monthly carrying cost, our Miami condo HOA breakdown covers the other half of that math. And for the 2026 property-tax picture — the third major line item after insurance and HOA — see our Florida Property Tax Guide.

The bottom line: Florida insurance is still expensive, but 2026 is the first year in a decade where the trajectory is down rather than up. If your premium didn't drop at renewal, shop. The market is finally letting you.

Broker One Editorial

Neighborhoods, Lifestyle & Buyer Guides

Broker One Editorial writes the neighborhood guides, lifestyle coverage, and buyer advice that help readers navigate South Florida real estate. We mix on-the-ground reporting with data from Broker One Research — if a restaurant is mentioned, someone on the team has eaten there; if a neighborhood is described, someone has walked it. Our editorial writers are licensed Florida real estate professionals, long-time South Florida residents, or both. Every lifestyle claim that can be verified with data is checked against our research team's datasets before publication.