Miami New Construction Condos 2026: 36% of 2024 Towers Still Sit Unsold (Plus the Full Pipeline)

The price you pay isn't the price they're asking

The Miami condo pipeline keeps growing: 25 marquee pre-construction towers are scheduled for delivery between 2026 and 2028, from the 791-unit Mercedes-Benz Places in Brickell to the 100-floor Waldorf Astoria Residences downtown. At the same time, more than a third of the towers that delivered in 2024 still haven't sold their units. We pulled every condo listing in the marquee zips of Miami-Dade and Broward, separated what's actively for sale from what has actually closed in the last 24 months, and the gap between those two prices is the most useful number a buyer can know in 2026.

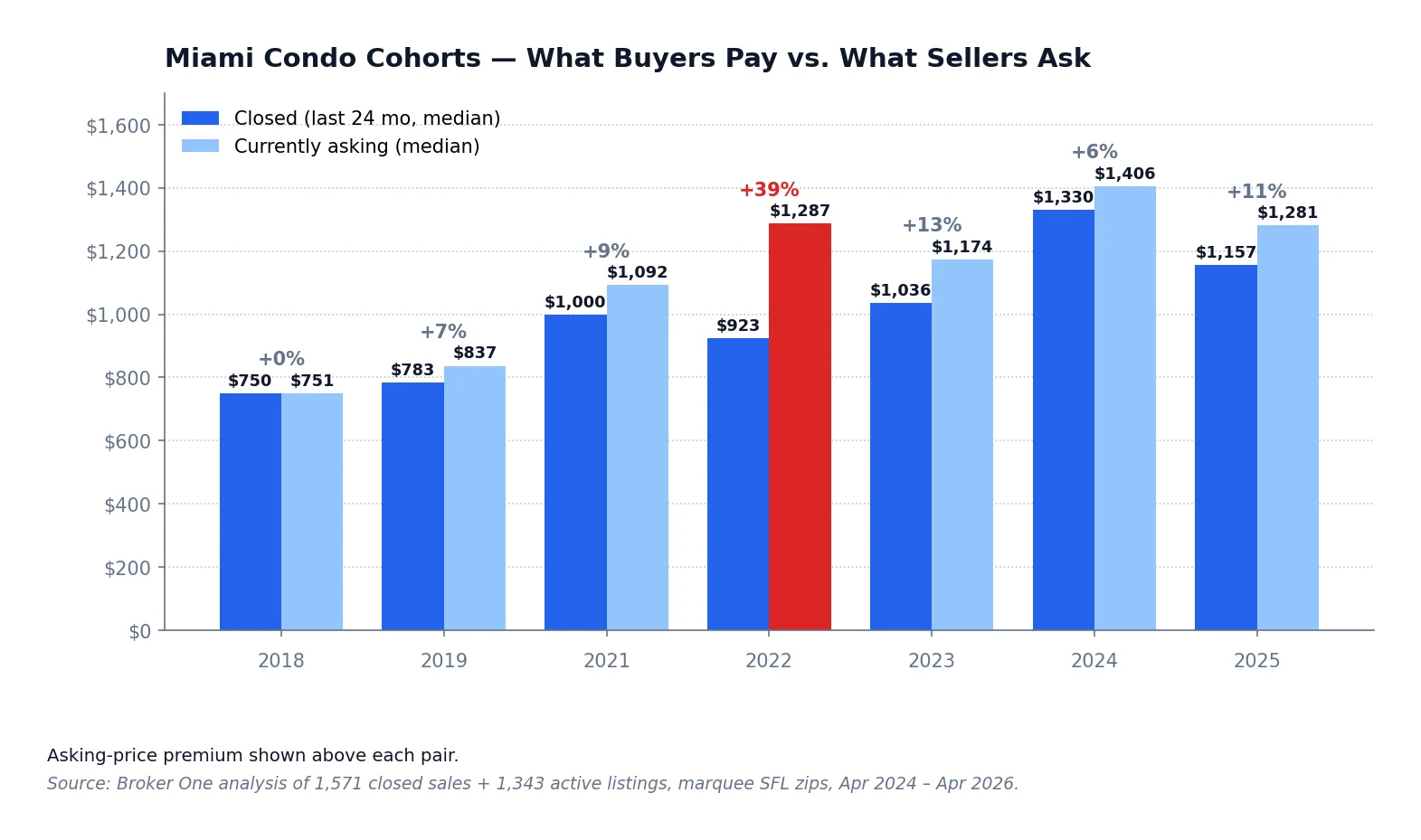

For the 2022-built condo cohort in South Florida, the median asking price is running 39% above the median closing price. Sellers want $1,287/sqft, buyers are clearing the market at $923/sqft, and the gap has barely budged in 18 months.

What buyers actually pay vs. what sellers ask

The single most important table in this post. Every row is the median price per square foot for South Florida condos in the marquee zips (33131-33180 plus the Fort Lauderdale Beach corridor), grouped by the year the building was completed. The "Closed" column reflects what units actually traded for in the last 24 months. The "Active" column reflects what's currently sitting on the market, unsold.

Closed vs. asking price per square foot, by year-built cohort. Source: Broker One analysis of 1,571 closed condo sales and 1,343 active listings in marquee SFL zips, April 2024 – April 2026.

Year built

Closed median $/sqft

Active asking median $/sqft

Ask premium

2018

$750

$751

0%

2019

$783

$837

+7%

2021

$1,000

$1,092

+9%

2022

$923

$1,287

+39%

2023

$1,036

$1,174

+13%

2024

$1,330

$1,406

+6%

2025

$1,157

$1,281

+11%

2026

insufficient closes

$1,449

—

2027 (pre-con)

—

$1,387

—

2028 (pre-con)

—

$1,480

—

Three things stand out. First, the 2018 cohort has reached price discovery: a six-year-old building has been bought, sold, refinanced, and re-listed enough times that asking and closing prices converge to the dollar.

Second, the 2022 cohort is stuck. These are buildings that delivered into the post-Surfside, post-rate-hike environment, where developers had already booked deposits at peak-2021 pricing. Sellers won't drop below the prices they signed for, buyers won't pay above what current comps actually clear at, and inventory keeps building in the 39-point gap.

Third, and this is the buyer's edge, the 2027 and 2028 pipeline is being priced above the 2024 closing median. Developers are asking $1,387–$1,480/sqft for product that won't deliver for 18-36 months, in a market where comparable freshly-delivered product clears at $1,330. The pre-construction "discount" that historically rewarded early buyers, typically 15-25% below comparable resale, has inverted.

The submarket reality check

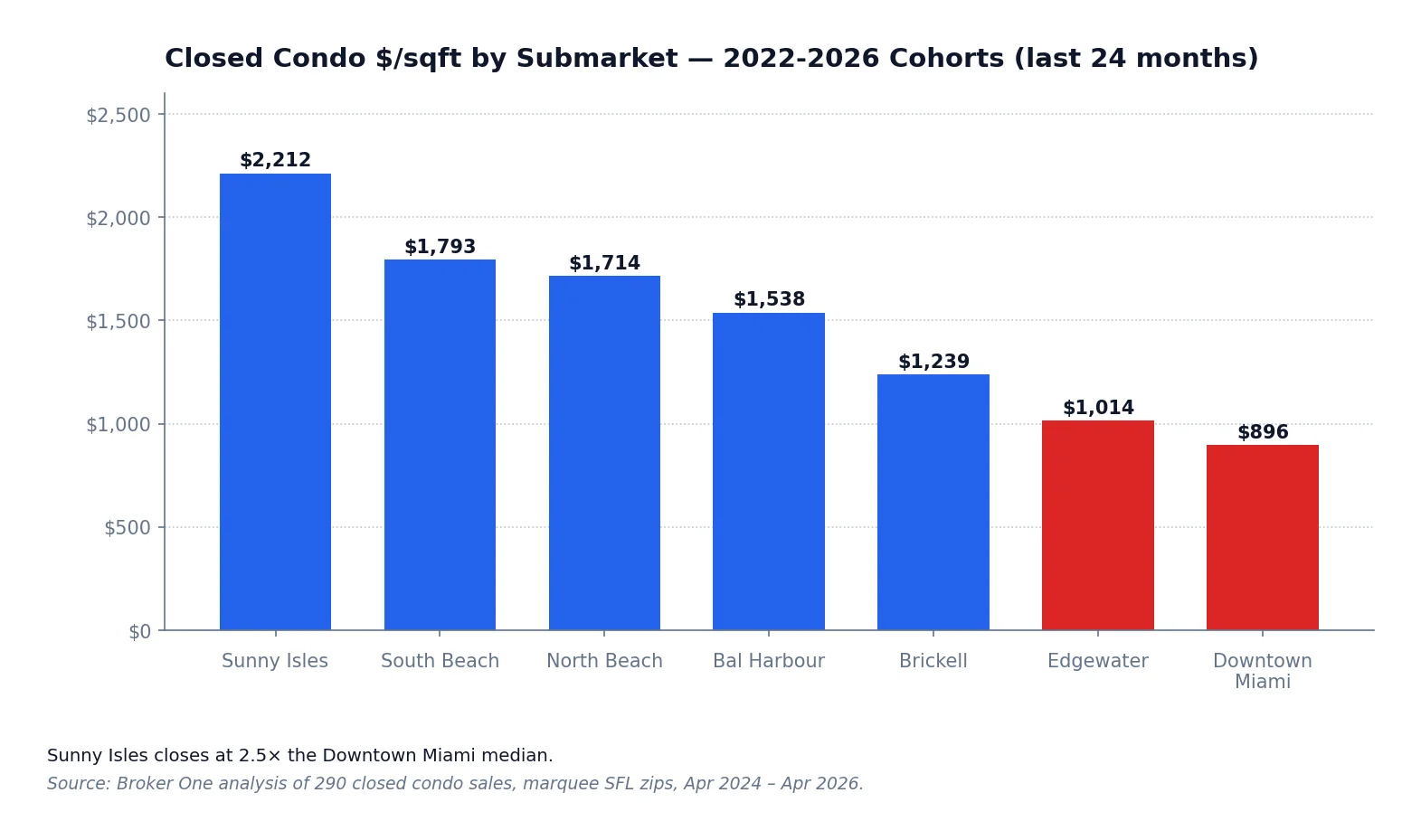

Aggregate numbers hide the geography. The same dollar of "Miami new construction" buys very different products depending on which mile of coastline you're standing on.

Median closed $/sqft by submarket for condos delivered 2022–2026, last 24 months. Source: Broker One analysis of 290 closed sales.

Highest density, deepest active inventory, hospitality-condo product mix

Two contrasts are doing all the work in this table. Sunny Isles Beach is the only submarket where ultra-luxury delivery is still being absorbed at premium PSF: closed deals run $2,212/sqft, more than 2.4× the Downtown Miami median of $896. The pipeline reflects that: the Bentley Residences, St. Regis Residences Sunny Isles, and South Tower at the Estates at Acqualina all sit on Collins Avenue oceanfront, and all are priced consistent with what already clears.

Downtown Miami is the opposite story. Of the condos completed in 2024 in zip 33132, 66% are still sitting active. The submarket ships the most pipeline by unit count and absorbs the least by share. Closed deals there clear at $896/sqft, one-third of what Sunny Isles closing buyers pay, yet the pipeline (Waldorf Astoria, Casa Bella, the Genting / Resorts World assemblage at 1015 N. American Way that pulled $63 million in 2026 permits) is priced as if Downtown were already a Sunny Isles substitute.

The 2026–2028 pipeline, by name

Twenty-five marquee pre-construction towers are currently being marketed for South Florida delivery in 2026–2028. We've covered each one individually; the table below ties them together with the data points buyers actually need.

Add it up: roughly 4,800 marquee-tier units coming to South Florida between 2026 and 2028, concentrated in the same submarkets that already have an absorption problem with what was delivered in 2024. The Brickell pipeline alone runs 1,800 units across six towers, all funneling into a submarket that closed the 2024 cohort at $1,239/sqft and currently has 33% of that cohort still unsold.

That figure understates the true pipeline. We only counted buildings with active marketing, MLS listings, and named developers. A second tier sits behind it: approved-but-unannounced projects, county permits being pulled (Downtown 33132 alone has booked $305 million in construction permits since 2022), and developer JVs that haven't gone public.

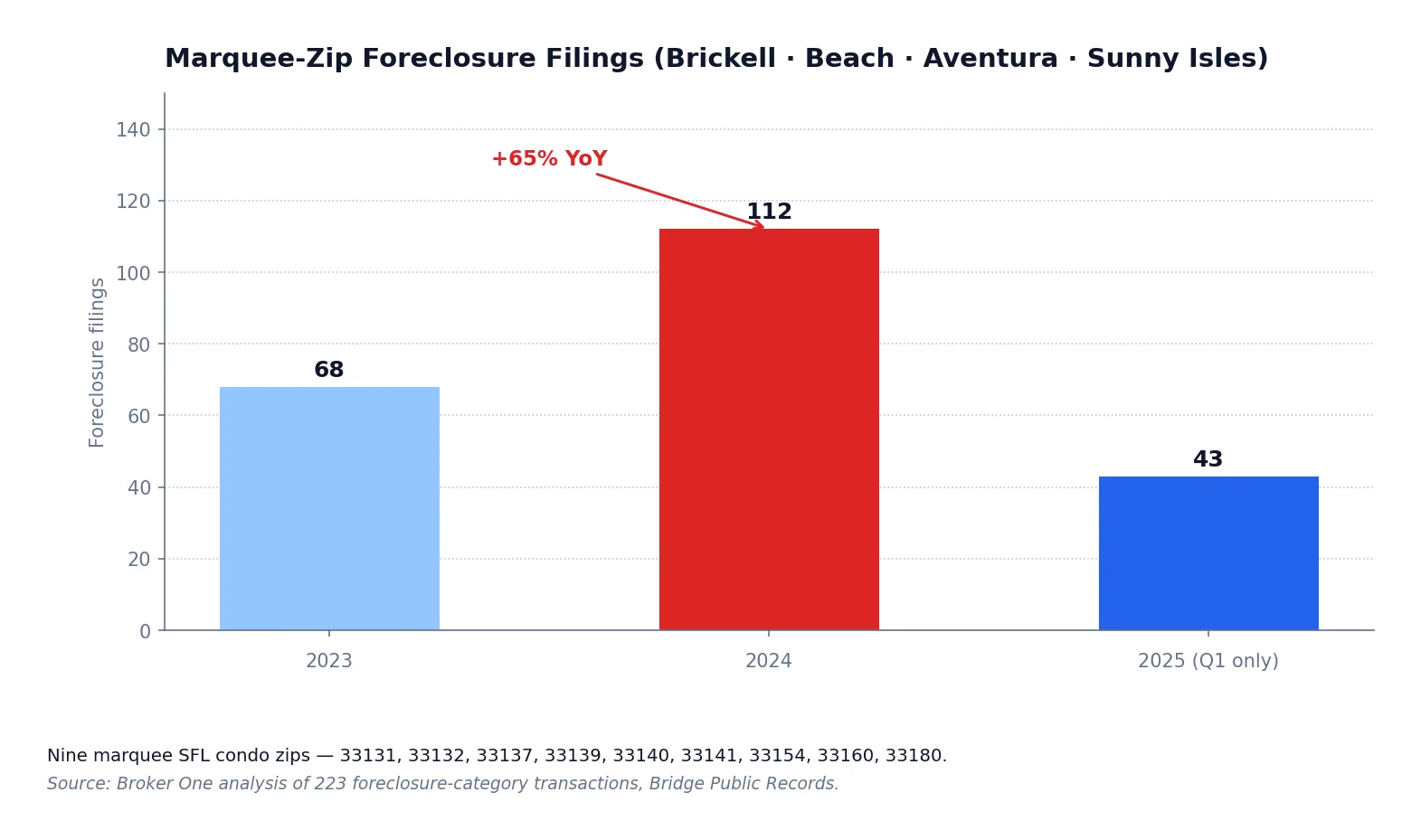

The distress signal nobody mentions

The other half of the absorption story is what happens to the inventory that doesn't sell. We pulled every foreclosure recorded in nine marquee SFL condo zips (Brickell through Aventura) since 2023, sourced from county-clerk filings and Bridge Public Records.

Foreclosure filings in marquee SFL condo zips. Source: Broker One analysis of 223 foreclosure-category transactions, 2023–April 2026.

Year

Marquee-zip foreclosures

YoY change

2023

68

—

2024

112

+65%

2025 (Q1 only)

43

roughly flat-to-down annualized

The 65% jump from 2023 to 2024 isn't 2008-style. It is, however, the largest single-year increase in marquee-zip condo foreclosures in the post-pandemic period, and it lands in the same neighborhoods where the absorption stall is sharpest. South Beach (33139) led with 22 foreclosure filings in 2024; North Beach (33141) had 19; Brickell (33131) had 17. Three of the nine zips accounted for more than half the volume.

The mechanism is straightforward. SB 4-D structural reserves kicked in, HOA fees stepped up across older buildings, insurance premiums repriced, and rate-locked owners who'd been carrying with thin margins started missing payments. Most of those filings will end in negotiated short sales rather than auction-block transfers, but every one of them adds inventory to a market that already has too much.

What this means if you're buying

The data doesn't say "don't buy a Miami condo in 2026." It says you have leverage you didn't have in 2022, and the leverage is concentrated in specific places.

If you're shopping resale, anchor your offers to the closed PSF column.

Sellers will quote asking prices that reflect optimism. Pull the closing comps from the last six months in the building, compute median PSF, and bid against that. The 2022 cohort is the highest-leverage starting point: sellers there are 39 percentage points anchored above the market.

If you're shopping pre-construction, demand a discount to comparable 2024 closes, not a premium.

The historical pre-con bargain (15-25% below resale comps) has inverted in the current pipeline. If a 2027 contract is being written above what the same submarket's 2024 product closes at, you're paying for delivery risk. Either negotiate the price down or extend the contingency window.

If you're shopping Sunny Isles, the math still works.

Direct-ocean ultra-luxury is the one segment where closed PSF still tracks asking PSF. The pipeline (Bentley, St. Regis Sunny Isles, Acqualina South Tower) priced for that reality.

If you're shopping Downtown Miami or Brickell mid-tier, wait or negotiate hard.

Two-thirds of the 2024 Downtown cohort hasn't closed; a third of the 2024 Brickell cohort hasn't closed. Sellers in those buildings are competing with developers still cutting tape on next year's product.

"Miami condo crash" is the headline you'll see most places. The data shows a repricing instead: a slow, friction-heavy process where sellers walk down toward what buyers will pay. We're roughly 40% of the way through it for the 2022 cohort and barely starting it for the 2026–2028 pipeline.

Frequently asked questions

Why aren't condos in Miami selling?

Two-thirds of new-construction Miami condos delivered in 2024 are still unsold because asking prices are running well above what comparable units actually close at. The 2022 cohort is the most extreme: sellers are asking a median of $1,287 per sqft while closed deals clear at $923. Until the gap narrows, inventory builds. Insurance, HOA reserves under SB 4-D, and rate-locked mortgages are all contributing to slower turnover, but the primary driver is the price disconnect.

Are Miami condo prices going down in 2026?

Asking prices have moved very little. Closing prices have moved more. The mechanism is selective: well-priced units close, mispriced units sit. Across South Florida marquee zips, the 2024 cohort closed-PSF median is $1,330 vs $1,406 asking, a 6% premium that sellers are slowly negotiating away. The 2022 cohort, where the asking premium is 39%, is where actual price reductions are concentrated. There is no broad crash; there is a slow, friction-heavy repricing in specific submarkets.

Is 2026 a good time to buy a condo in Miami?

Yes if you understand the leverage. Buyers in Downtown Miami, Brickell mid-tier, and 2022-cohort buildings have the strongest negotiating position in years. Sellers there are competing with both other resale inventory and developers cutting tape on next year's product. Sunny Isles ultra-luxury still trades closer to asking, so leverage is weaker there. Pre-construction contracts being written today for 2027–2028 delivery should be negotiated below comparable 2024 closings, not above them.

How many new condos are being built in Miami?

Roughly 4,800 marquee-tier units across 25 named pre-construction towers are scheduled for delivery in South Florida between 2026 and 2028. Brickell alone has six towers totaling about 1,800 units in the pipeline, including Mercedes-Benz Places (791 units), Lofty Brickell (422), Baccarat Residences (324), 888 Brickell by Dolce & Gabbana (259), Mandarin Oriental Residences (228), and St. Regis Residences Brickell (152). The figure understates the true pipeline because it only includes projects with active marketing and named developers.

What is the absorption rate for new Miami condos?

Absorption varies sharply by submarket. Across South Florida, 36% of 2024-built condos are still active in the MLS as of April 2026, or 398 units of a 1,112-unit cohort. Submarkets vary: Downtown Miami's 2024 cohort is 66% unsold, Brickell's 2024 cohort is 33% unsold, while Sunny Isles 2022-2023 cohorts are closer to 25% unsold and clearing at premium PSF. Historically, condo cohorts five years past delivery hold around 6% inventory; the 2024 cohort is six times that level.

Are pre-construction Miami condos a good investment?

It depends on the price discipline. The historical pre-construction discount of 15–25% below comparable resale has inverted in the current market. Many 2027 and 2028 contracts are being written above what the same submarket's 2024 product closes at. That removes the cushion that traditionally compensated buyers for delivery risk and a 25–30% deposit lock-up. Direct-ocean Sunny Isles ultra-luxury still prices consistent with closing comps; mid-tier urban product is the segment where the math has the hardest time penciling.

What does the foreclosure data say about Miami condos?

Foreclosure filings in nine marquee South Florida condo zips jumped from 68 in 2023 to 112 in 2024, a 65% year-over-year increase. South Beach (33139) led with 22 filings; North Beach (33141) had 19; Brickell (33131) had 17. The trend is concentrated in older buildings facing stepped-up SB 4-D structural reserve assessments and higher insurance premiums, not in newly delivered towers. Most filings will end in negotiated short sales rather than auctions, but every one of them adds inventory to a market that already has too much.

Broker One Research is the data-journalism arm of Broker One. Every post under this byline is backed by an original SQL analysis across our proprietary datasets: 2M Florida parcels from county appraisers, 4.6M active and historical MLS listings, 6.9M Florida business entities from Sunbiz, FEMA flood zones, building permits, code violations, and Census ACS demographics. We publish our methodology — row counts, filters, date ranges — so readers can evaluate the rigor of every finding. We use median-based metrics rather than means to keep MLS data-entry outliers out of headline numbers. If you're a journalist or researcher who wants to cite our work, email research@mybrokerone.com.

")